State of Trade 2023: Inclusive Trade

ISSN 2562-8321

Table of contents

- Message from the Minister

- Executive summary

- Part 1: 2022 in review

- Part 2: Inclusive trade

- Acknowledgements

- Bibliography

Message from the Minister

I am excited to present Canada's State of Trade 2023 on behalf of the Government of Canada.

Despite the year's challenges, Canadian trade reached record highs again in 2022. This year, the report highlights Canada's inclusive approach to trade, our progress, and the results it brings. As we build on this momentum, we recognize that trade works best when everyone benefits.

Even with Russia's illegal and unjustified invasion of Ukraine last year, which has caused a horrific humanitarian crisis and sent economic shockwaves around the world, global trade has remained resilient. Canada continues to uphold and promote rules-based trade, providing confidence and predictability for our businesses.

Both exports and imports reached record levels, with Canada's two-way goods and services trade expanding to nearly $1.9 trillion in 2022. Throughout the year, supply chain pressures eased, creating increased opportunity for investment in vehicle manufacturing, among other sectors. In addition, services trade has surpassed its pre-pandemic levels, helping tourism and transportation trade see strong growth.

With all this positive momentum, we are building on our commitment of diversifying trade and creating more opportunities for Canadian businesses — including those owned by women, Black and other racialized entrepreneurs, Indigenous Peoples, members of the 2SLGBTQI+ community, and young people — to benefit from international trade. Take the Indo-Pacific Strategy, for example, which received support in Budget 2023. The Strategy will help Canadians and businesses benefit from engagement with the fastest-growing region in the world. It will create good jobs and inclusive opportunities on both sides of the Pacific.

The State of Trade 2023 shares our latest research and understanding of how small and medium enterprises (SMEs), women, Indigenous Peoples, and other diverse groups engage in international trade. This understanding guides our trade policies and shapes the customized supports we offer through our Trade Commissioner Service. As the momentum of our economic recovery continues — and as our economic resilience grows — it is critical to ensure that everyone can benefit from building a stronger, more sustainable and more secure Canadian economy. That's why our government will continue to create opportunities that open doors for Canadians and Canadian businesses around the world.

The Honourable Mary Ng

Minister of Export Promotion, International Trade and Economic Development

Executive summary

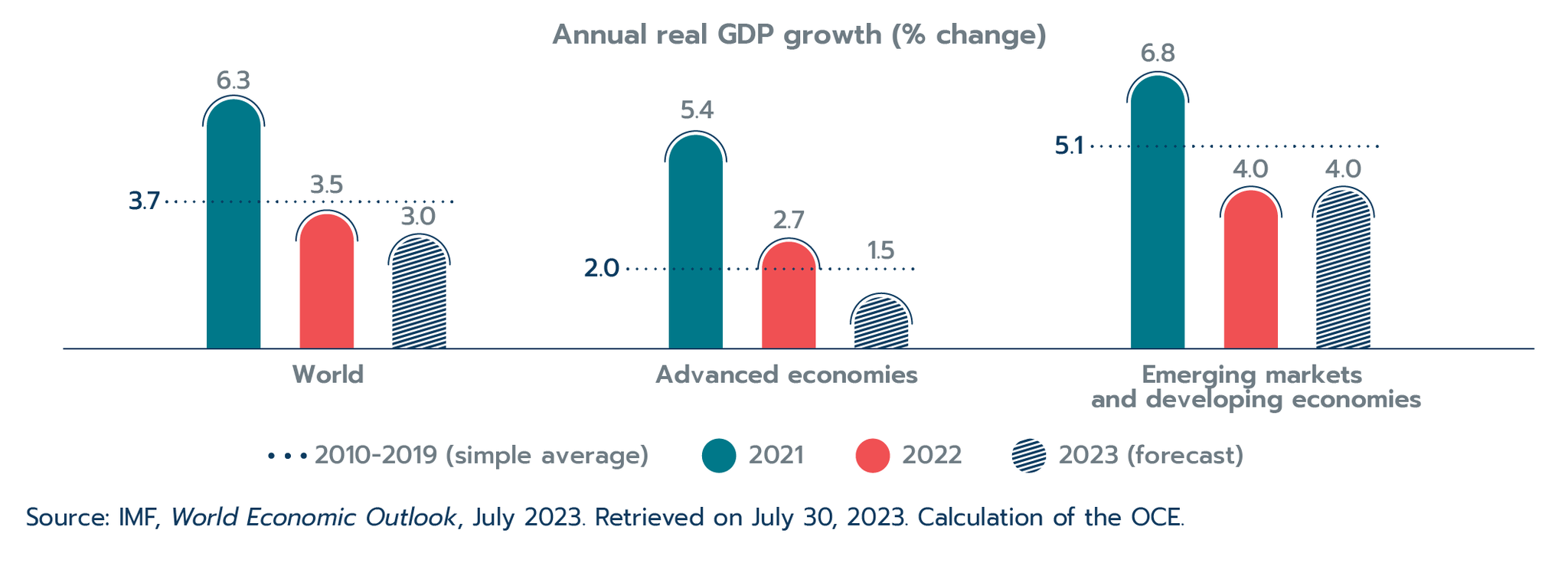

The global and Canadian economies continued to adapt to the realities of COVID-19 while new challenges emerged in 2022. The year 2022 began with the Omicron variant continuing to slow progress toward the full reopening of many economies, affecting China particularly hard. February 2022 brought further turmoil as Russia began its illegal invasion of Ukraine. The war led to immense human tragedy and economic challenges, including soaring commodity prices. This added fuel to the fire of rising global inflation, which peaked in 2022. The good news stories – including the continued administration of COVID-19 vaccines, the reopening of borders, the easing of supply chain issues, and strong demand – helped keep the global economy afloat. Nonetheless, the slowdown was widespread. Advanced economies, and emerging markets and developing economies saw growth slow to 2.7% and 4.0% in 2022, respectively. Overall, global economic growth advanced by 3.5% in 2022, following the 6.3% rebound witnessed in 2021.

In Canada, economic growth kept pace with the rest of the world. The Canadian economy expanded by 3.4% in 2022, although the expansion came to a halt and the economy contracted in the final quarter of the year as heightened inflation affected interest-rate-sensitive sectors. Indeed, the Bank of Canada had raised interest rates to 4.25% by the end of 2022 in response to inflation reaching a 40-year high on an annual average basis. Meanwhile, a robust labour market – with unemployment at an over 45-year low – supported consumer spending throughout 2022.

Canada's services industries grew faster, at 3.7%, than goods industries, at 3.4%, in 2022. Services growth was led by professional and technical services and public-facing industries, such as accommodation and food services, which benefited from the removal of COVID-19-related restrictions. Goods industries growth was widespread, with manufacturing posting the strongest contribution to growth as supply-chain challenges brought on by the pandemic and semi-conductor shortages eased.

With a surge in commodity prices and a strong U.S. economic performance, Canadian trade broke records for the second year in a row. Canada's goods and services exports increased by 21.2% to reach $940.4 billion in 2022. In part due to the war in Ukraine, commodity prices soared such that Canadian resource products accounted for over three-quarters of goods export growth. Overall, price increases drove the advance in goods exports, and to a lesser extent in goods imports, in 2022. The removal of COVID-19-related restrictions helped growth in services exports, led by travel services. However, travel services remain below their pre-pandemic levels.

Canada's goods and services imports advanced 20.5% to reach $936.2 billion in 2022. Growth in consumer goods, energy products and vehicles led goods import growth, while travel services dominated the services import expansion.

Canada's two-way international investment flows slowed in 2022, following a significant rebound in 2021. Direct investment flows into Canada contracted by 21.5%, while Canadian direct investment abroad decreased by 15.8%. Canadian investment flows followed the overall trends in global investment in 2022. Nevertheless, both inward and outward investment flows remained above their average levels seen in the pre-pandemic decade (2010–2019).

Canada is a trading nation, and trade brings many benefits to businesses, workers and consumers. However, we cannot take for granted that these benefits will automatically flow to everyone. The State of Trade 2023 features inclusive trade research by the Office of the Chief Economist (OCE). Inclusive trade research is centered on understanding how women, Indigenous and other racialized people, youth, 2SLGBTQI+, and small and medium enterprises (SMEs) benefit from trade and investment. The focus is on identifying both the challenges and success strategies for underrepresented groups in going global to inform policies and programs designed to ensure that everyone has the opportunity to benefit from Canada's international trade.

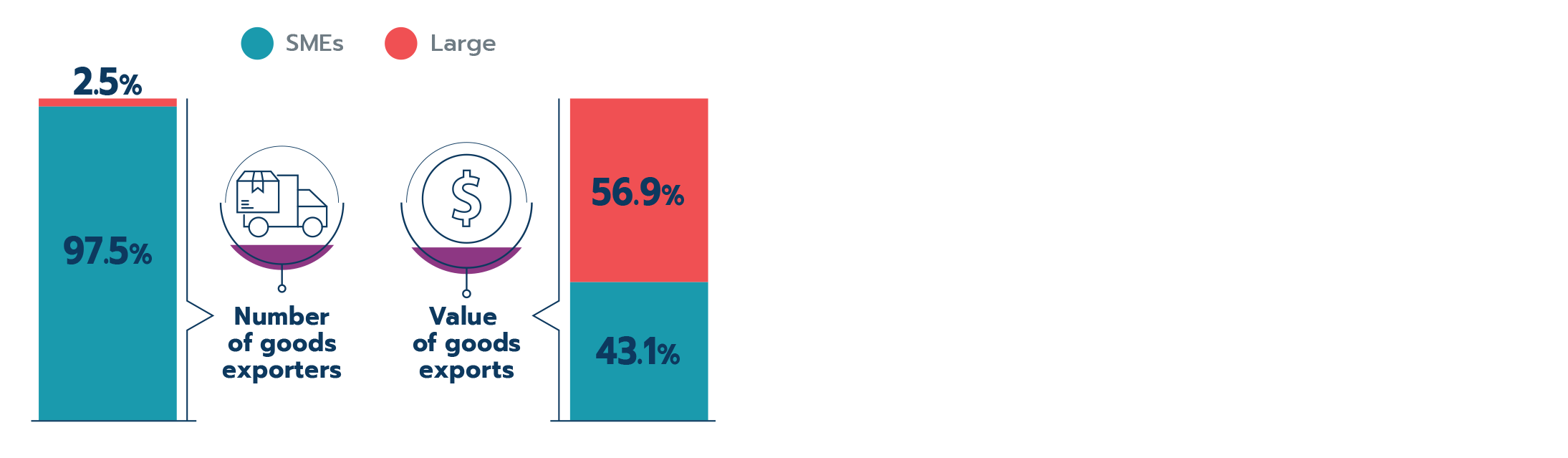

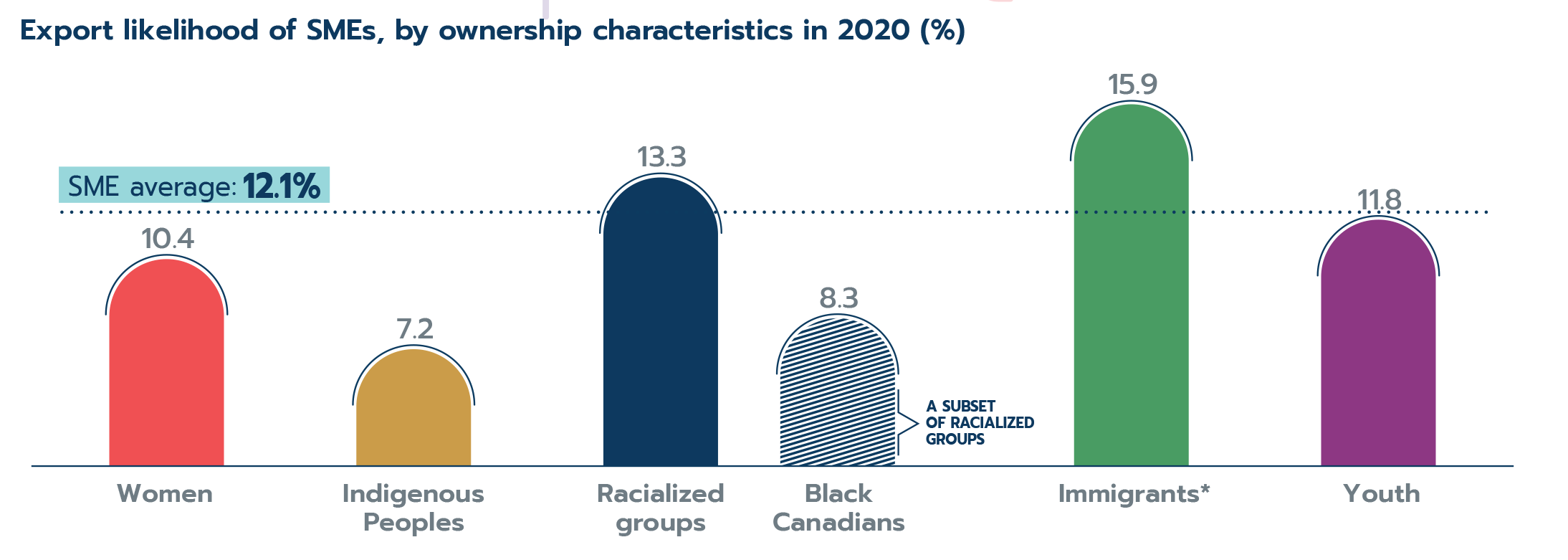

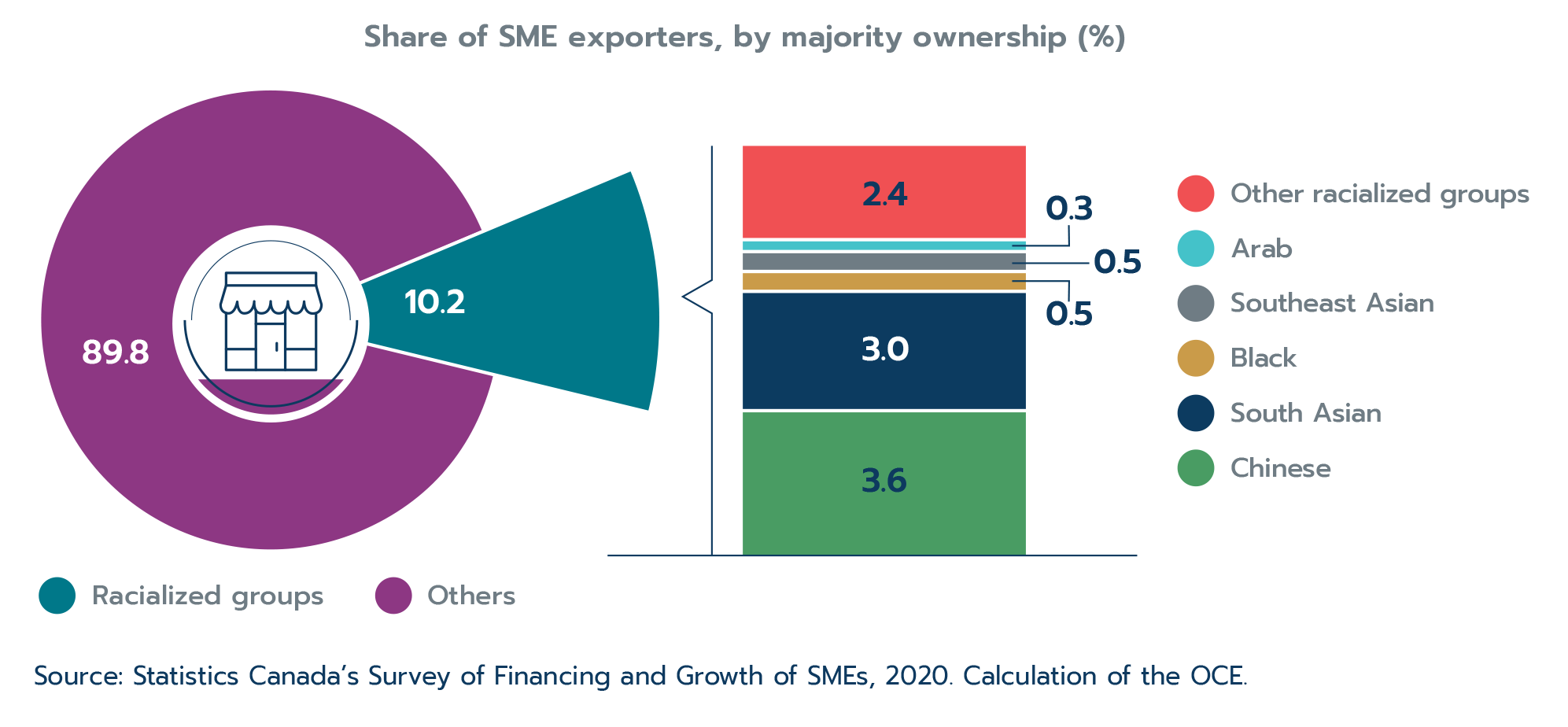

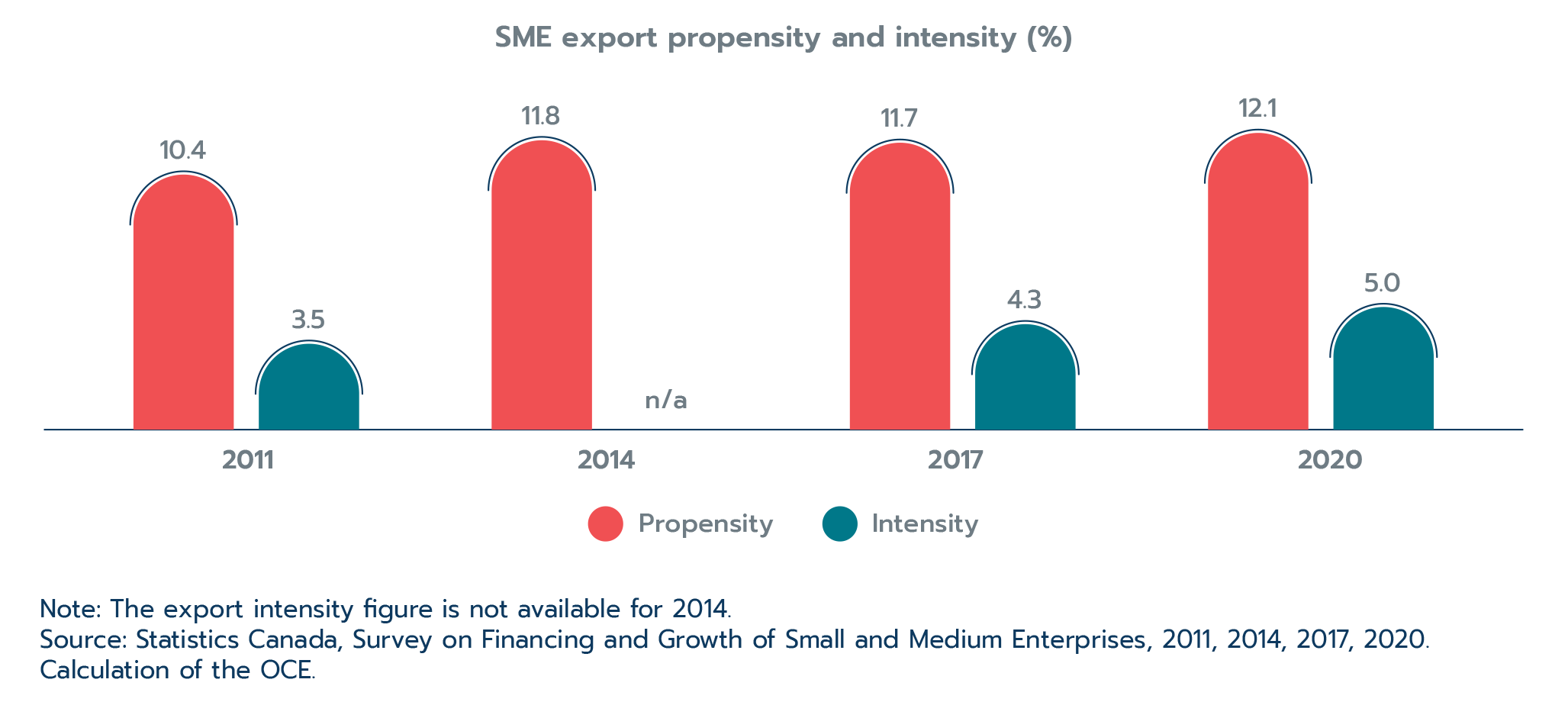

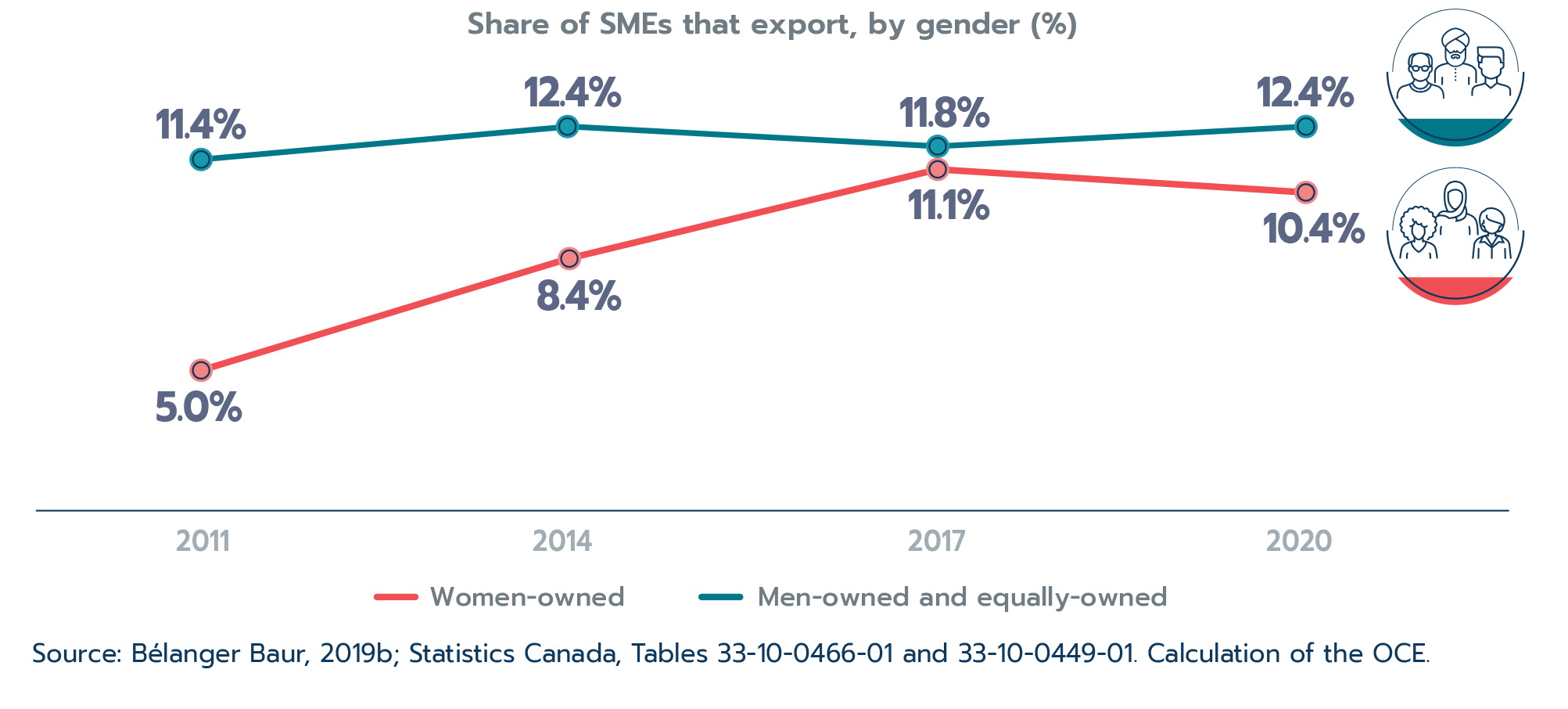

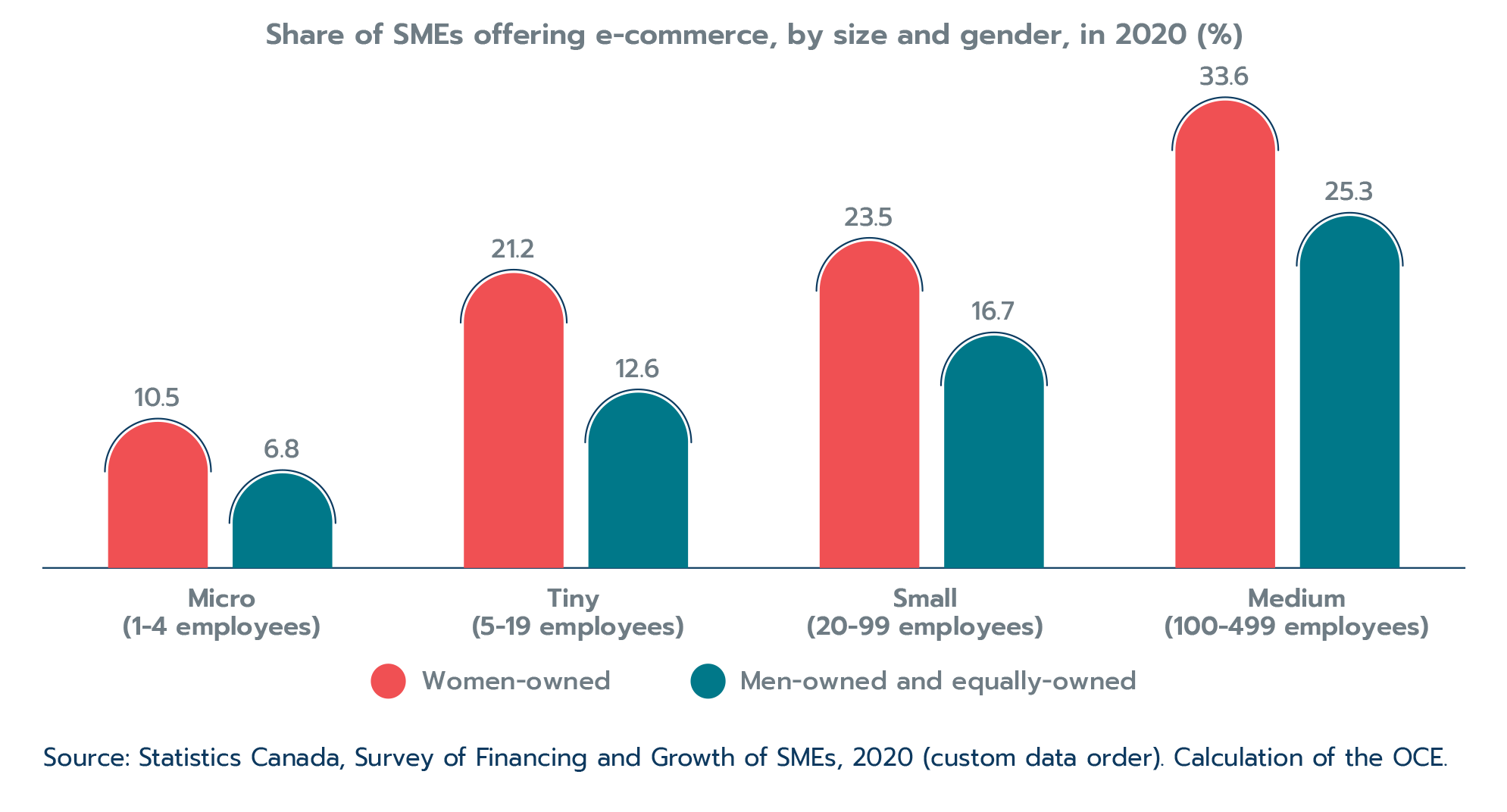

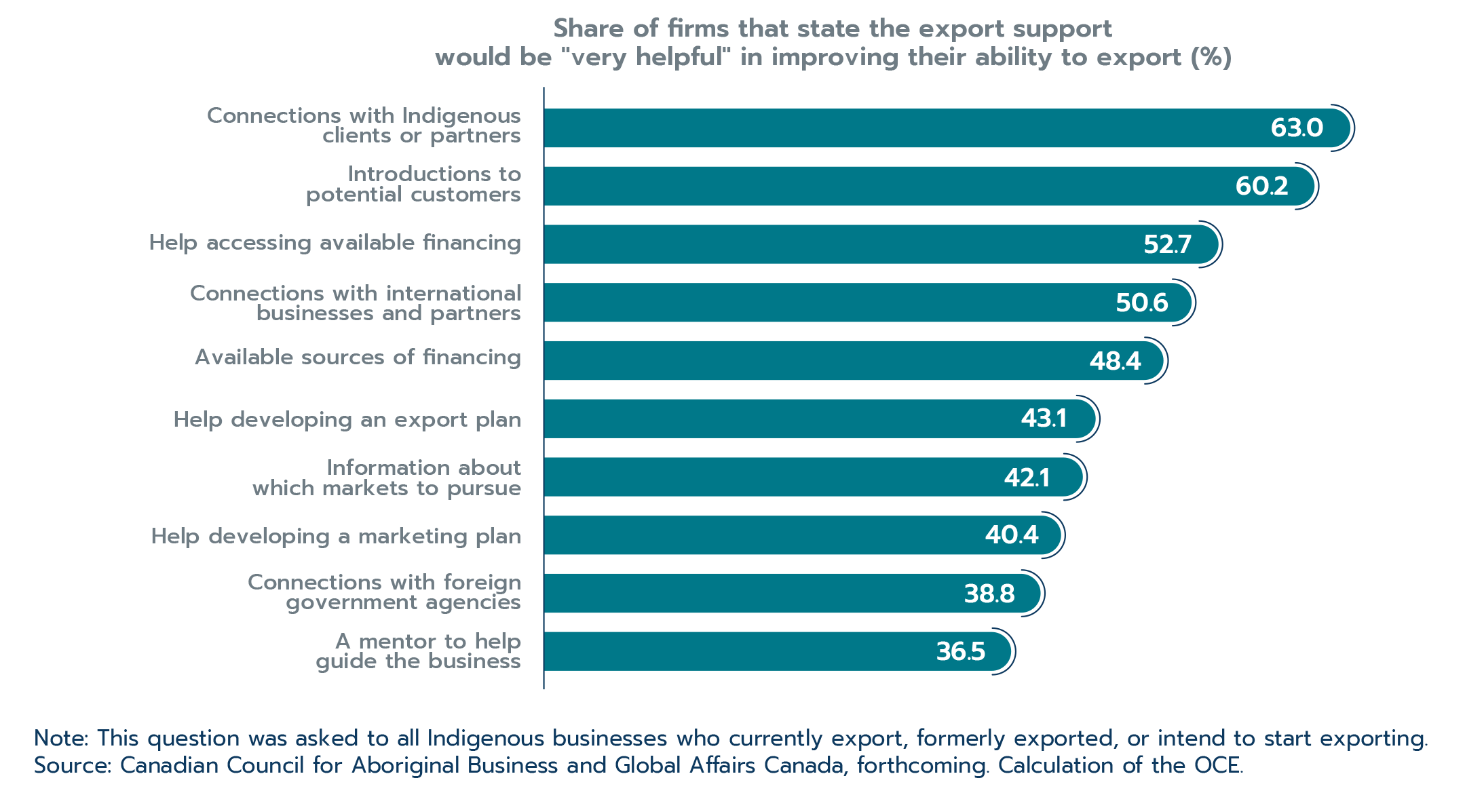

OCE's inclusive research reveals Canada's progress on the inclusive trade front. Canadian SMEs were more likely to export in 2020 (12.1%) than they were a decade ago (10.4%), and the share of their revenues coming from export sales has increased. In the same timeframe, women-owned SMEs more than doubled their likelihood to export, from 5.0% to 10.4%. Recent OCE work in partnership with the Canadian Council for Aboriginal Business emphasizes that Indigenous-owned SMEs put a strong focus on global markets, and finds that Indigenous women-owned SMEs tend to export at similar rates to Indigenous men-owned SMEs.

Another part of Canada's inclusive trade strategy involves a quantitative assessment of the inclusive elements under a trade agreement. The OCE conducts this analysis both before and after trade policies are implemented. Economic modelling conducted before negotiations reveals net positive gain for workers, including women, associated with the implementation of free trade agreements. Analysis of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP)'s first year of implementation reveals that Canadian SMEs increased their dutiable goods exports to new CPTPP markets by 12.3%, while SMEs with high export growth increased their hiring of women by 11.4%.

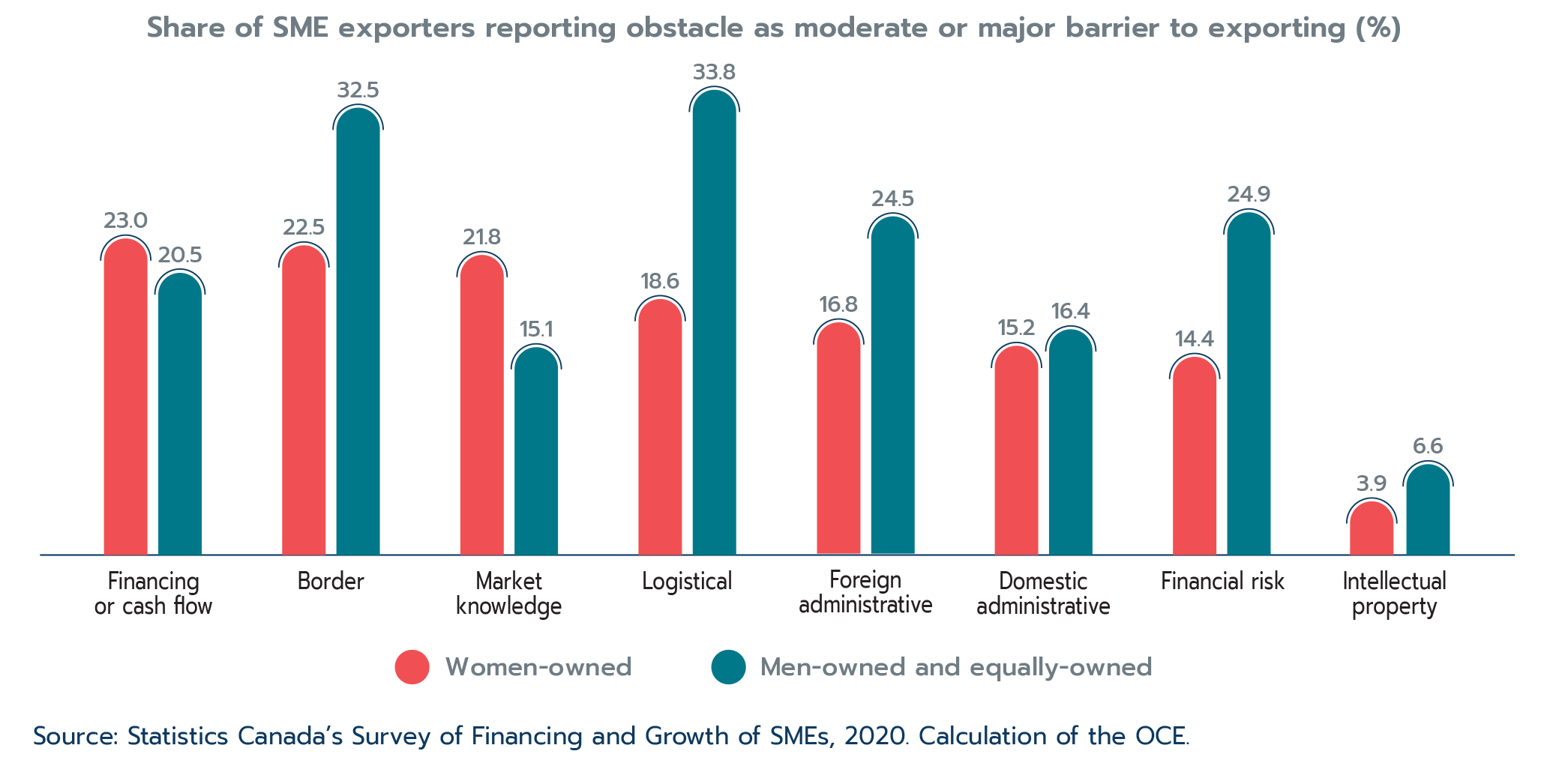

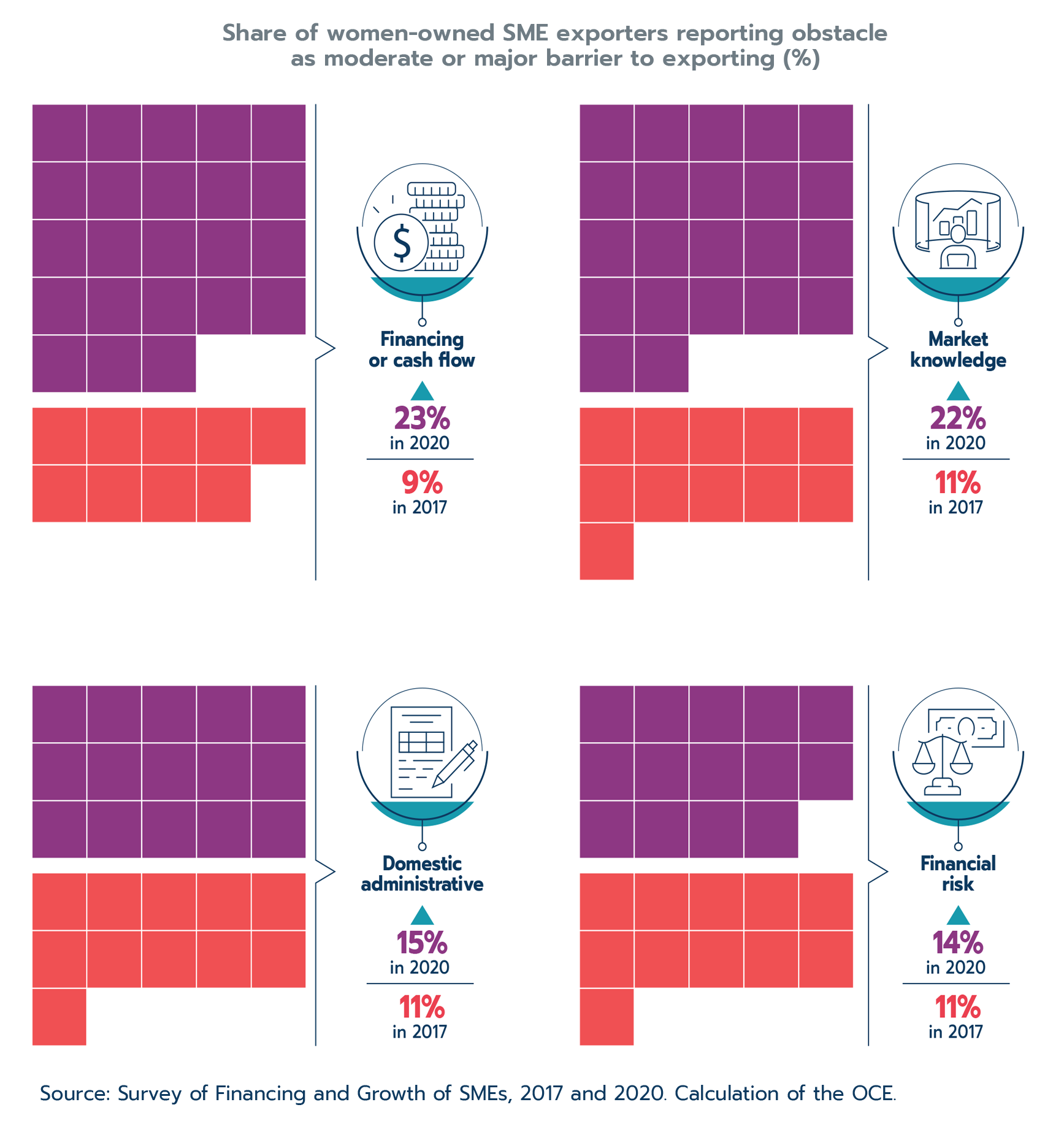

While the expanded involvement of underrepresented groups in trade signifies meaningful progress, we know that gaps remain. For example, SMEs—particularly Indigenous-owned SMEs—are underrepresented among exporting firms, and women-owned SMEs are less export intensive. OCE research has identified specific challenges facing each of these groups, ranging from a lack of market knowledge among women to difficulties in obtaining access to financing and a lack of digital and physical infrastructure for Indigenous entrepreneurs.

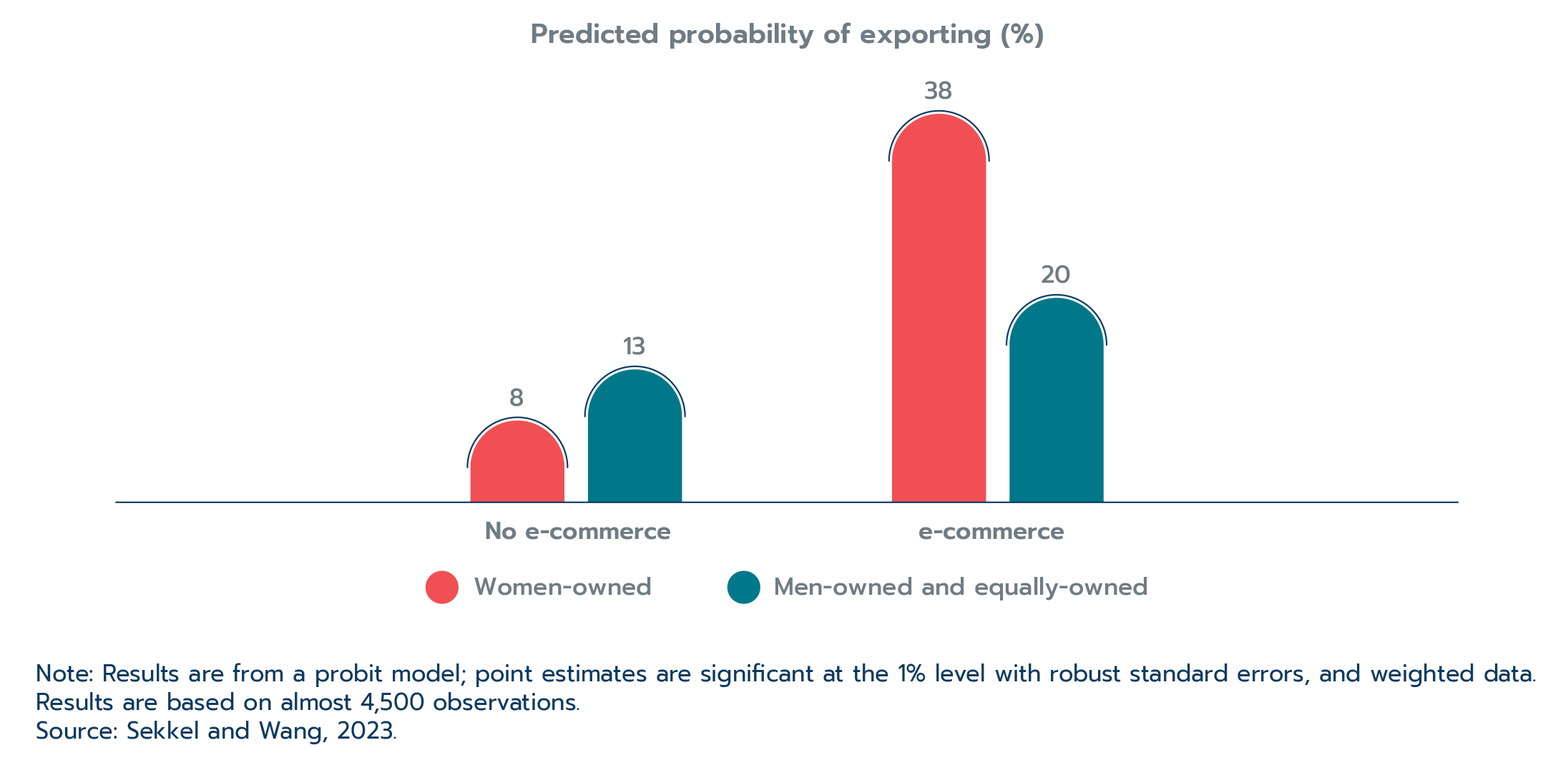

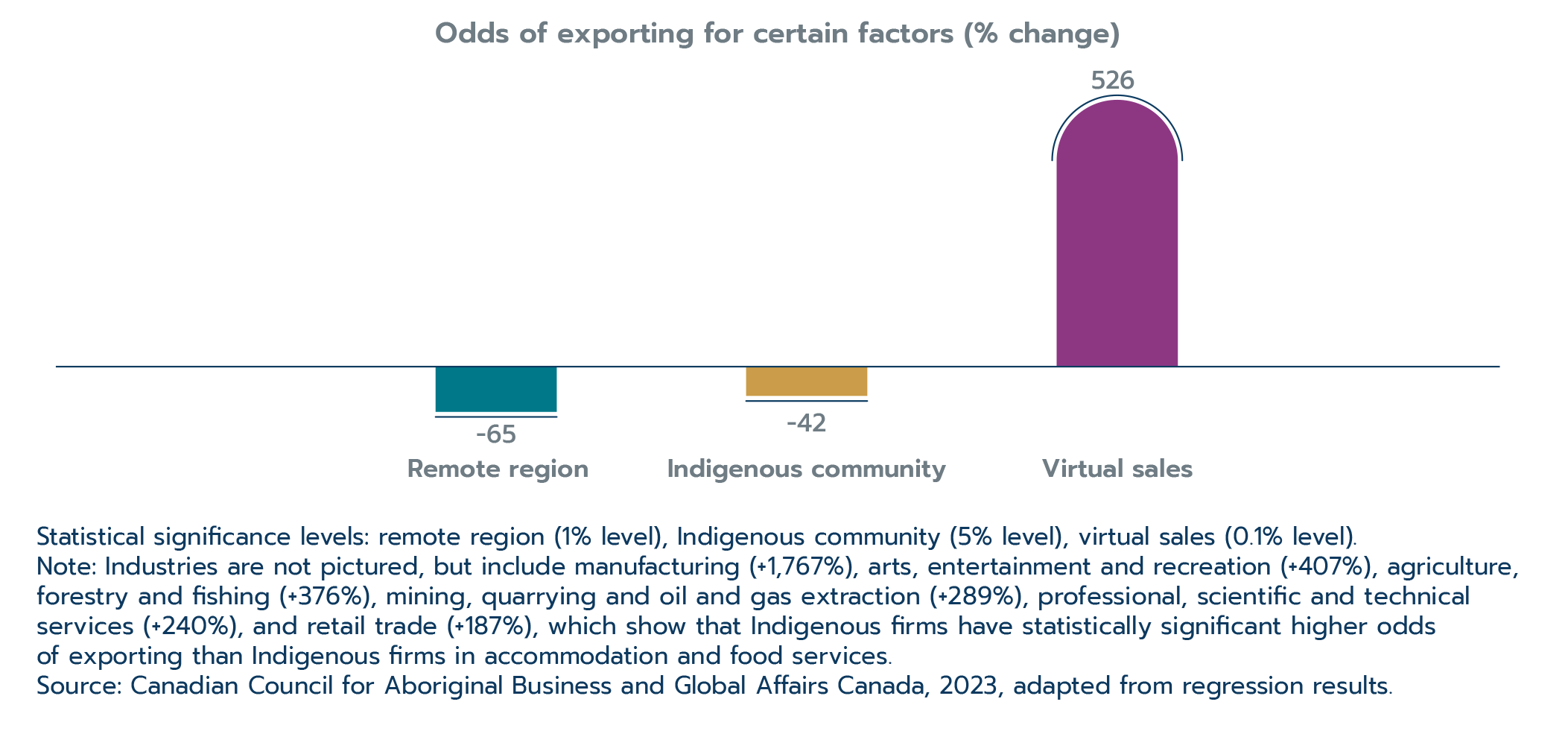

Importantly, OCE research has also uncovered enabling factors and successful strategies. For example, SMEs using e-commerce are 13.1% more likely to export, with an even stronger effect for women-owned SMEs (Sekkel and Wang, forthcoming). Virtual sales are also important for Indigenous-owned SMEs and are associated with a six-fold increase in the odds of exporting (Canadian Council for Aboriginal Business and Global Affairs Canada, 2023).

With this enhanced understanding, Global Affairs Canada is providing support to underrepresented groups to participate fully in international trade by continuing to ensure that trade agreements specifically reflect the needs of these groups, by offering customized programs through its Trade Commissioner Service, and by working across government to develop evidence-based policies and programs for these groups. This work recognizes that an inclusive trade approach is not a zero-sum game; increased participation in trade by more groups generates broader economic opportunities and prosperity for all Canadians.

Part 1: 2022 in review

Part 1: At a glance

Global economic growth slowed in 2022 amidst continued waves of COVID-19, the war in Ukraine, and rising inflation and interest rates – growth will slow further in 2023.

- Global growth slows: As global inflation reached decade highs, economic growth slowed to 2.7% in advanced economies and 4.0% in emerging markets and developing economies in 2022.

- The International Monetary Fund expects global growth to slow from 3.5% in 2022 to 3.0% in 2023.

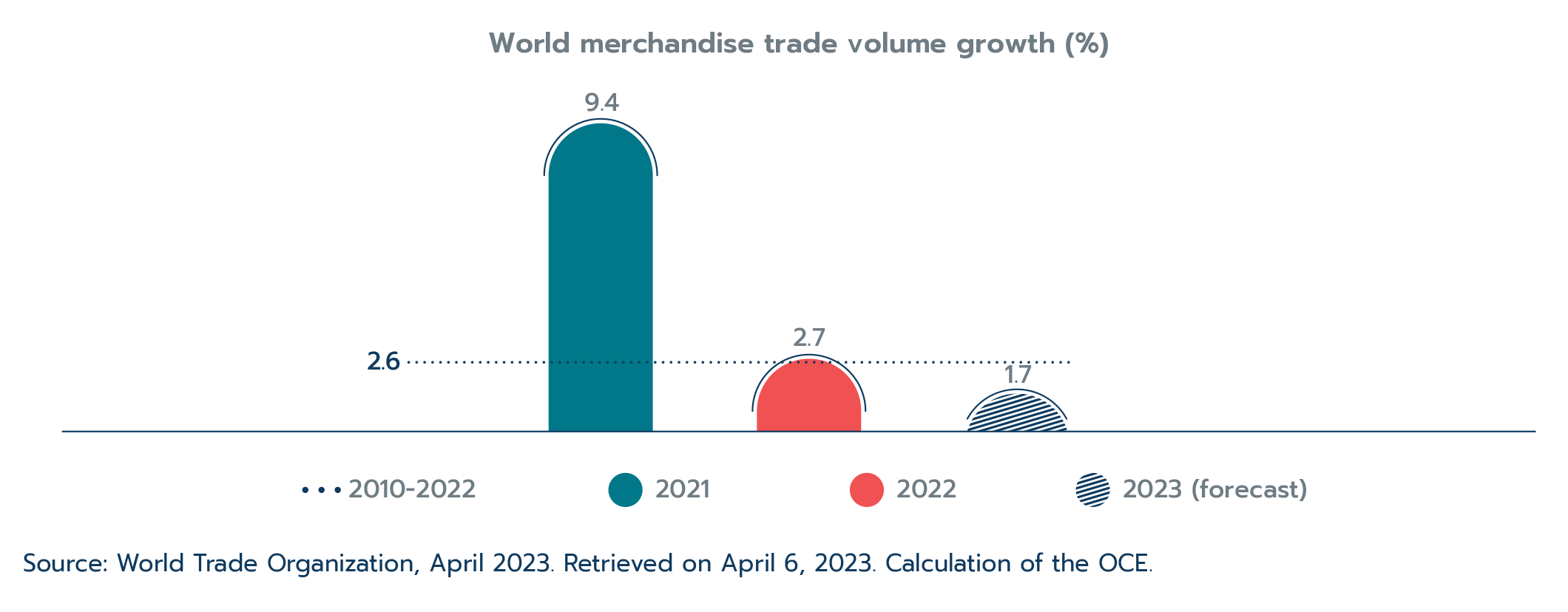

- Trade holds up: World merchandise trade volumes (up 2.7%) fared better than expected in 2022, but growth slowed toward the end of the year, dragged down by waves of COVID-19, the war in Ukraine, high commodity prices, and tightened monetary policy.

Text version

Global real GDP:

- 2021: 6.3%

- 2022: 3.5%

- 2023: 3.0%

Canadian economic performance was robust in 2022, advancing 3.4% – compared to its G7 peers, Canada has seen the second strongest recovery from the pandemic shock.

- Services led growth: Services industries – helped by the removal of COVID-19-related restrictions – led Canadian growth in 2022, expanding by 3.7%.

- Goods growth continues: Growth in goods industries (3.4%) was robust in 2022, supported by the easing of supply-chain issues and high commodity prices, among other factors.

- Tight labour markets: The Canadian labour market was historically tight in 2022, with low unemployment (5.3%) and high employment and job vacancies.

- Record inflation: Inflation reached a 40-year high at 6.8% in 2022. This led the Bank of Canada to raise its target rate to 4.25 % – the highest in nearly 15 years.

Text version

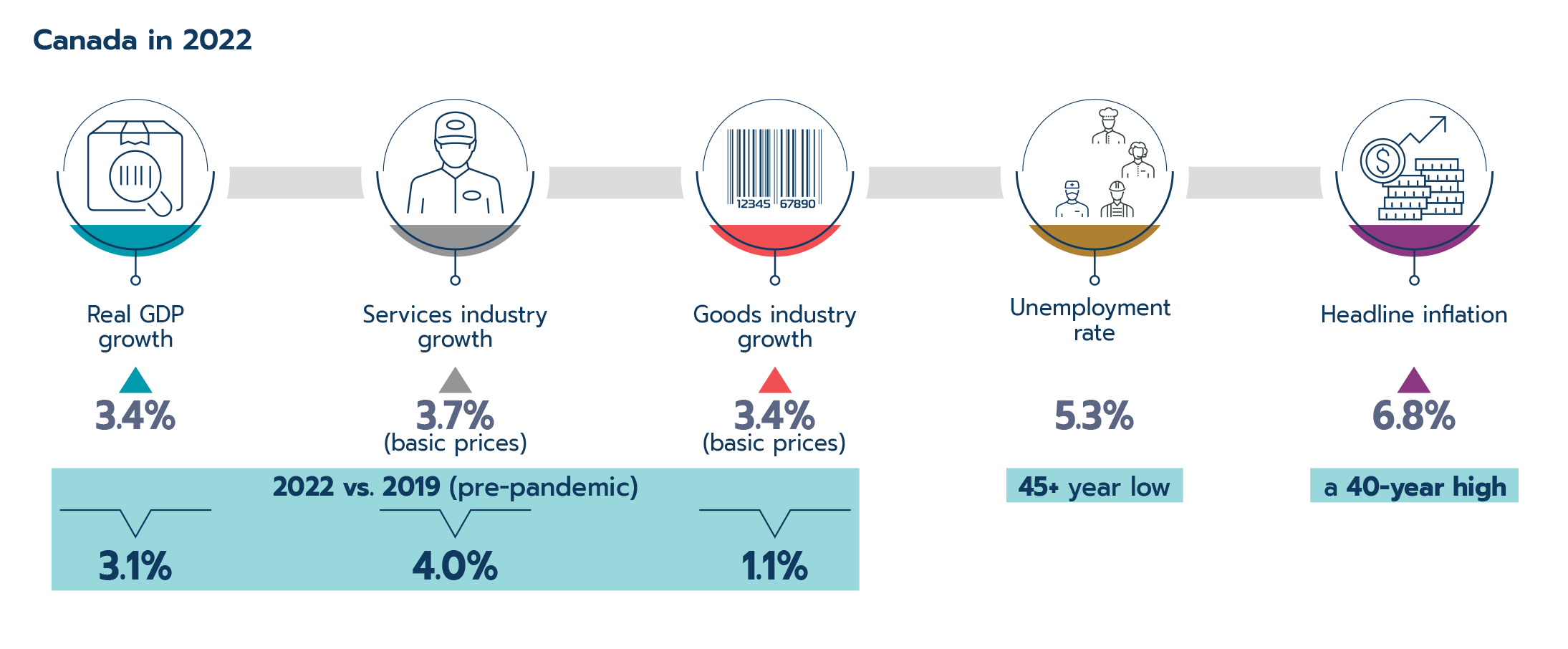

Canada in 2022

- Real GDP growth: 3.4%

- +3.1% versus 2019 (pre-pandemic)

- Services industry growth: 3.7% (basic prices)

- +4.0% versus 2019 (pre-pandemic)

- Goods industry growth: 3.4% (basic prices)

- +1.1% versus 2019 (pre-pandemic)

- Unemployment rate: 5.3% (an over 45-year low)

- Headline inflation: 6.8% (a 40-year high)

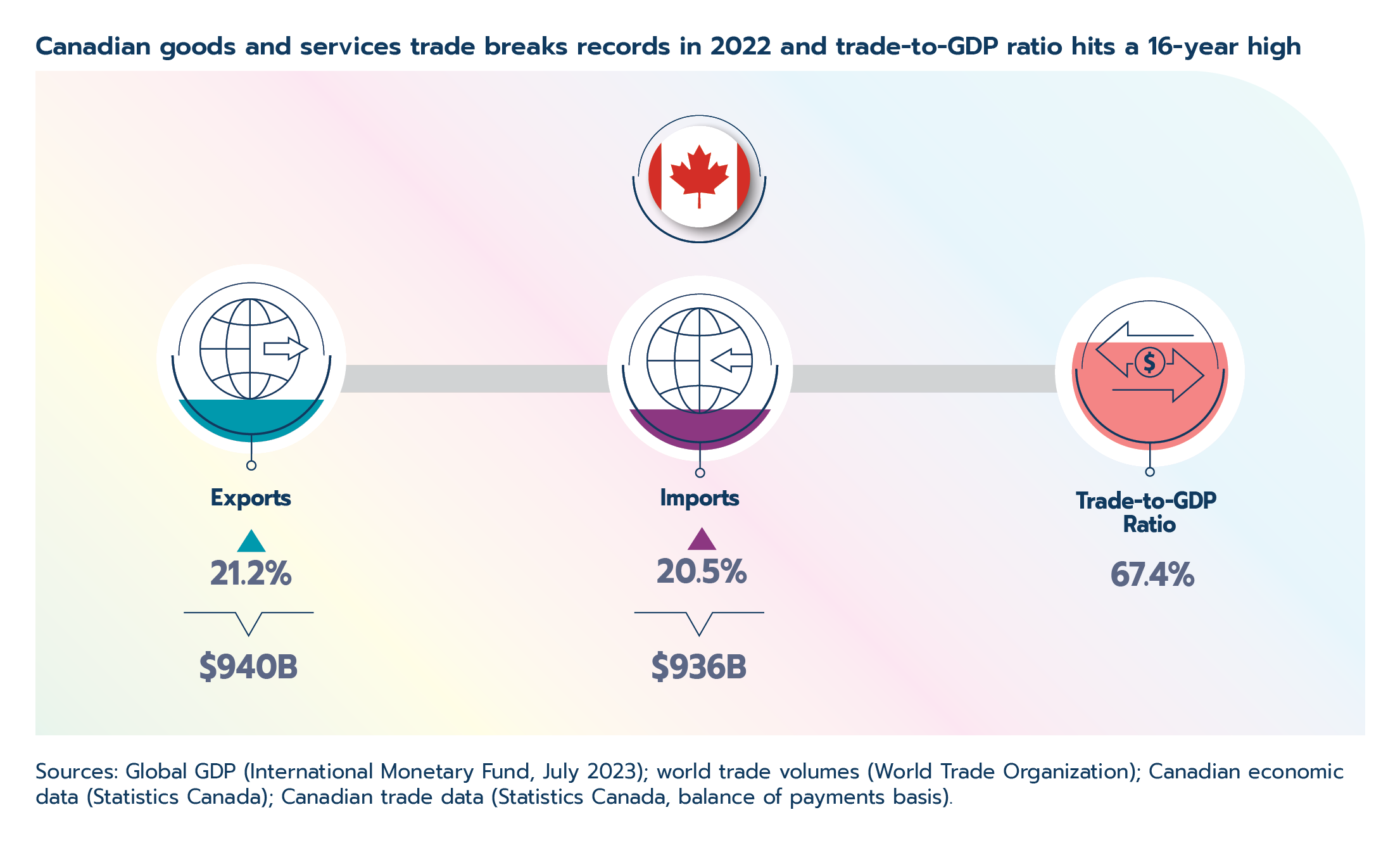

Canadian exports and imports reached record highs – two-way goods and services trade reached nearly $1.9 trillion in 2022. Canada is also back on track to meet its export diversification targets.

- Record trade: Led by energy products, Canadian goods and services exports increased by 21.2% in 2022. Meanwhile, goods and services imports expanded by 20.5%.

- With the elimination of Canada's COVID-19-related restrictions in 2022, services exports and imports surpassed their 2019 levels, while goods exports and imports had already done so the year before.

- Trade with Russia collapses: In response to the war in Ukraine, Canada implemented sanctions on trade with Russia, resulting in a significant annual drop in merchandise exports (-67.2%) to and imports (-64.5%) from that country in 2022.

- Investment slows: Canada's two-way international investment flows declined in 2022. Trade and transportation drove the contraction in investment abroad while a decline in other industries, manufacturing, and energy and mining led the investment contraction in Canada.

- Nevertheless, international investment inflows and outflows remain above their pre-pandemic historical average (2010–2019).

- 2023 slowdown: The challenges that emerged in 2022 are expected to slow global growth in 2023; Canadian trade and investment are likely to follow suit.

Text version

Canadian goods and services trade breaks records in 2022 and trade-to-GDP ratio reached a 16-year high

- Exports: $940 billion (+21.2%)

- Imports: $936 billion (+20.5%)

- Trade-to-GDP ratio: 67.4%

1.1 Introduction

During the course of 2022, most countries lifted the last of the public health measures implemented to stop the spread of COVID-19. This helped spur growth in sectors hit hardest by the pandemic, as did the easing of supply chain challenges. At the same time, however, goods and services prices soared in 2022, and Russia’s invasion of Ukraine in February 2022 dishearteningly marked the start of the biggest armed conflict in Europe since World War 2. The war has already had incalculable costs and continues to wage on. In brief, two simultaneous stories marked 2022: one of continued economic recovery and the other of rising macroeconomic and geopolitical challenges.

While the year began on an optimistic note of strong economic growth, it ended with widespread expectations of recessions in advanced economies and forecasts of slowing global growth. In Part 1 of the State of Trade 2023 report, we look back at the events that unfolded in the global and Canadian economies in 2022, focusing on trends in trade and investment.

1.2 Global context

Several positive developments supported global growth in 2022. An increasing number of vaccine doses were administered throughout the year, helping to save lives and increase confidence in the safety of in-person activities. Most countries also removed or relaxed their COVID-19-related restrictions that inhibited in-person services and travel throughout the prior two years, igniting a recovery in several industries. Moreover, supply chain issues that peaked at the end of 2021, including the semiconductor shortage, eased during 2022, which supported growth in industries like vehicle manufacturing.

Unfortunately, factors inhibiting global growth outweighed those supporting it in 2022. Just a few short months into the year, Russia invaded Ukraine, devastating the lives of millions of people and weighing on global economic activity. In addition, the COVID-19 Omicron variant constrained growth in advanced and emerging markets at the start of the year. In China, ongoing lockdowns muted economic growth all year. Possibly the most important factor, advanced and emerging markets alike experienced decades-high inflation in 2022. Compared to the International Monetary Fund’s estimate of average inflation in the decade before the pandemic (2010‒2019), inflation in advanced economies and emerging markets and developing economies was nearly five times and two times higher, respectively, in 2022. In response to record inflation, central banks around the world began tightening monetary policy at a rapid rate.

Overall, the global economy grew by 3.5% in 2022, slightly below the IMF’s estimated 3.7% average annual growth between 2010 and 2019 and significantly lower than the 4.4% growth forecasted in their January 2022 report. Advanced economies and emerging markets contributed to the slowdown. Advanced economies expanded by 2.7% in 2022 compared to 5.4% in 2021, while emerging markets advanced 4.0% in 2022 compared to 6.8% in 2021 (Figure 1.1).

Figure 1.1: Economic growth slowed in advanced economies and emerging markets

Text version

Annual real GDP growth (% change)

| Average 2010‒2019 | 2021 | 2022 | 2023 (forecast) | |

|---|---|---|---|---|

| World | 3.7 | 6.3 | 3.5 | 3.0 |

| Advanced economies | 2.0 | 5.4 | 2.7 | 1.5 |

| Emerging markets and developing economies | 5.1 | 6.8 | 4.0 | 4.0 |

Source: IMF, World Economic Outlook, July 2023. Retrieved on July 30, 2023. Calculation of the OCE.

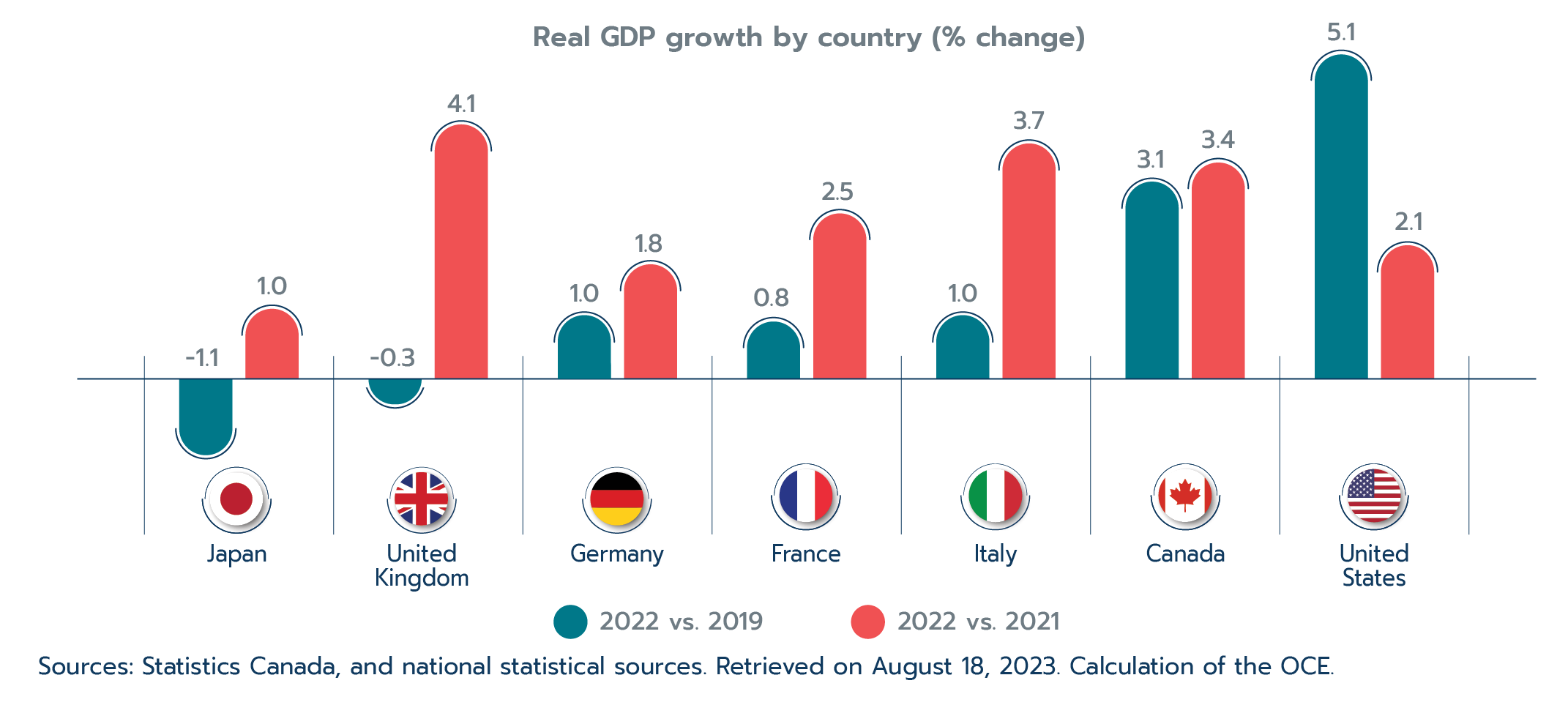

In advanced economies, growth in the Euro area (3.5%) surprised on the upside, posting a slightly faster-than-average growth rate in 2022. Despite the challenges brought on by the war in Ukraine, private consumption and fixed capital investment powered ahead, albeit with some loss of momentum in the region during the second half of the year as high energy prices and the fallout from the war took their toll. The United States slowed sharply in 2022 compared to 2021, growing by only 2.1%, as inflation and tightened financial conditions outweighed the positive impacts of robust labour markets and strong consumer spending. Inflation, contracting investment, and weak exports plagued Japanese economic growth, which slowed to 1.0% in 2022.

In emerging markets, continued lockdowns linked to COVID-19 through much of the year and challenges in its property market dragged down growth in China. The year 2022 marked the first time in more than 40 years that China’s economy expanded at a slower rate than the global average. Tight global financial conditions and the increasing cost of goods and services, particularly for energy and food, pulled down growth in other emerging markets and developing economies overall. Energy price strength supported decades-high economic growth in energy exporters such as Kuwait and Saudi Arabia, while slowing growth in net energy import markets, such as India and Mexico.

Global trade and investment

Global trade proved resilient in the face of 2022’s challenges. World merchandise trade volumes increased by 2.7% overall in 2022 (Figure 1.2), which is roughly in line with the World Trade Organization’s (WTO) estimate of trade growth between 2010 and 2022, and is close to their April 2022 forecast. Stronger than expected spending in many advanced economies, the easing of supply chain issues, and the success of countries in finding alternative suppliers for goods impacted by the war (e.g., gas, cereals, wheat) all helped to avoid a faster deceleration of trade in 2022 (WTO, 2023). Trade volume growth was significantly slower in the final quarter of the year as the impacts of the war in Ukraine, high commodity prices, continued COVID-19 outbreaks, and tightening monetary policy acted in concert.

Figure 1.2: World trade volumes grow steadily despite macroeconomic and geopolitical challenges

Text version

World merchandise trade volume growth (%)

| Average 2010‒2022 | 2021 | 2022 | 2023 (forecast) | |

|---|---|---|---|---|

| Merchandise trade volume growth | 2.6 | 9.4 | 2.7 | 1.7 |

Source: World Trade Organization, April 2023. Retrieved on April 6, 2023. Calculation of the OCE.

Like global trade, global investment appears to have held up overall in 2022 but showed signs of struggle in the second half of the year. Preliminary data from the United Nations Conference on Trade and Development (UNCTAD) shows that greenfield investment was up marginally at the end of the year while cross-border mergers and acquisitions (M&A) contracted slightly. Amidst rising interest rates and financial market uncertainty, M&A sales worldwide decreased by roughly 6.0%; especially notable was the decrease of over 50% in U.S. M&A sales. Furthermore, many Western multinationals announced departures or suspension of activities in Russia in response to its invasion of Ukraine.Footnote 1 On the upside, several mega-projects were announced in the renewables industry (in response to increasing climate concerns) and in the semiconductors industry (reflecting the reconfiguration of supply chains) (UNCTAD, 2023).

Looking ahead

The world emerged from 2022 with added sources of uncertainty that will continue to plague the outlook for 2023. The IMF expects global economic growth to slow to 3.0% in 2023, following the 3.5% growth posted in 2022 (Figure 1.1). The challenges that emerged in 2022, including tightening financial conditions and the war in Ukraine, will continue to drag down growth and could potentially worsen. Moreover, if the instability in financial markets observed at the beginning of 2023 spreads further, it could worsen the already challenging global macroeconomic environment.

The IMF forecasts a more severe slowdown in advanced economies, with growth reduced by almost half to 1.5% in 2023, the lowest rate of growth since 2013, excluding the contraction caused by the initial shock of the COVID-19 pandemic in 2020. Growth in the Euro area will fall to 0.9% in 2023 from 3.5% in 2022 as the war in Ukraine continues and higher interest rates take hold. Notably, a full recession is expected in Germany (-0.3%), which remains vulnerable to energy price volatility and will be negatively impacted by weak foreign demand. Inflation and high interest rates are expected to trigger a slowdown in U.S. economic growth (1.8%) and the United Kingdom (0.4%).

Growth in emerging markets will stay at 4.0% in 2023. After lifting its zero-COVID policy in December 2022, China's reopening will support growth in emerging markets. Economies in emerging Europe are also expected to support growth. Meanwhile, slowdowns in Latin America, the Middle East, and Sub-Saharan Africa, will pull down growth. Debt vulnerabilities continue to cloud the outlook for over half of low-income developing economies and about a quarter of emerging market economies (IMF, 2023).

With global growth decelerating, the WTO forecasts global trade growth will slow to 1.7% in 2023, markedly lower than the 3.9% annual average rate seen between 2010 and 2019. Additionally, UNCTAD predicts that FDI is likely to weaken in 2023, mirroring global economic and trade growth.

1.3 Canadian economic performance

The year 2022 was marked by another strong performance for the Canadian economy, which advanced by 3.4% following the 5.0% growth posted in 2021. Despite robust headline growth, the economy contracted by the end of 2022 as the Bank of Canada raised interest rates to contain accelerating inflation.

Despite the negative impacts brought on by the spread of Omicron and associated containment measures, the Canadian economy grew by 2.6% (seasonally adjusted at annual rates) in the first quarter of 2022. Another two quarters of robust expansion followed, with the economy increasing by 3.6% and 2.3% in the second and third quarters, respectively.

Strong labour and housing markets and government stimulus from the pandemic that continued into 2022 supported growth in consumption during the first three quarters of the year. However, the Canadian economy stalled by the fourth quarter of 2022, contracting by 0.1% as interest-rate-sensitive sectors began to falter. A significant contraction in inventories and business investment in housing and machinery and equipment outweighed positive contributions from consumption and net exports in the fourth quarter.

Throughout the year, inflation continued to accelerate, driven by robust consumer demand and elevated commodity prices following Russia's invasion of Ukraine in February of 2022. Halfway through the year, Canada's headline inflation reached a 40-year high on an average annual basis. Goods and services inflation were too high, averaging 8.7% and 5.0% in 2022, respectively.

Correspondingly, the Bank of Canada tightened monetary policy. The policy interest rate increased by 4 percentage points during the year, ending 2022 at a 15-year high of 4.25%. On a more positive note, supply-chain pressures significantly decreased in 2022, nearing their pre-pandemic norms, which provided some relief for goods price growth.

Canada was not alone in this experience, with most major economies seeing record inflation and increasing interest rates throughout the year. Nonetheless, two consecutive years of solid growth pushed the Canadian economy beyond its pre-pandemic size – Canada’s real GDP was 3.1% greater in 2022 compared to 2019, reaching $2.2 trillion. This is the second-strongest performance among G7 nations, behind only the United States. (Figure 1.3).

Figure 1.3: Canada posts second-strongest recovery among G7 countries

Text version

Real GDP growth by country (% change)

| 2022 vs. 2019 | 2022 vs. 2021 | |

|---|---|---|

| Japan | -1.1% | 1.0% |

| United Kingdom | -0.3% | 4.1% |

| Germany | 1.0% | 1.8% |

| France | 0.8% | 2.5% |

| Italy | 1.0% | 3.7% |

| Canada | 3.1% | 3.4% |

| United States | 5.1% | 2.1% |

Sources: Statistics Canada, and national statistical sources. Retrieved on August 18, 2023. Calculation of the OCE.

Industry performance

Economic growth was widespread in 2022 – with every major industry advancing, except for management of companies and enterprises.

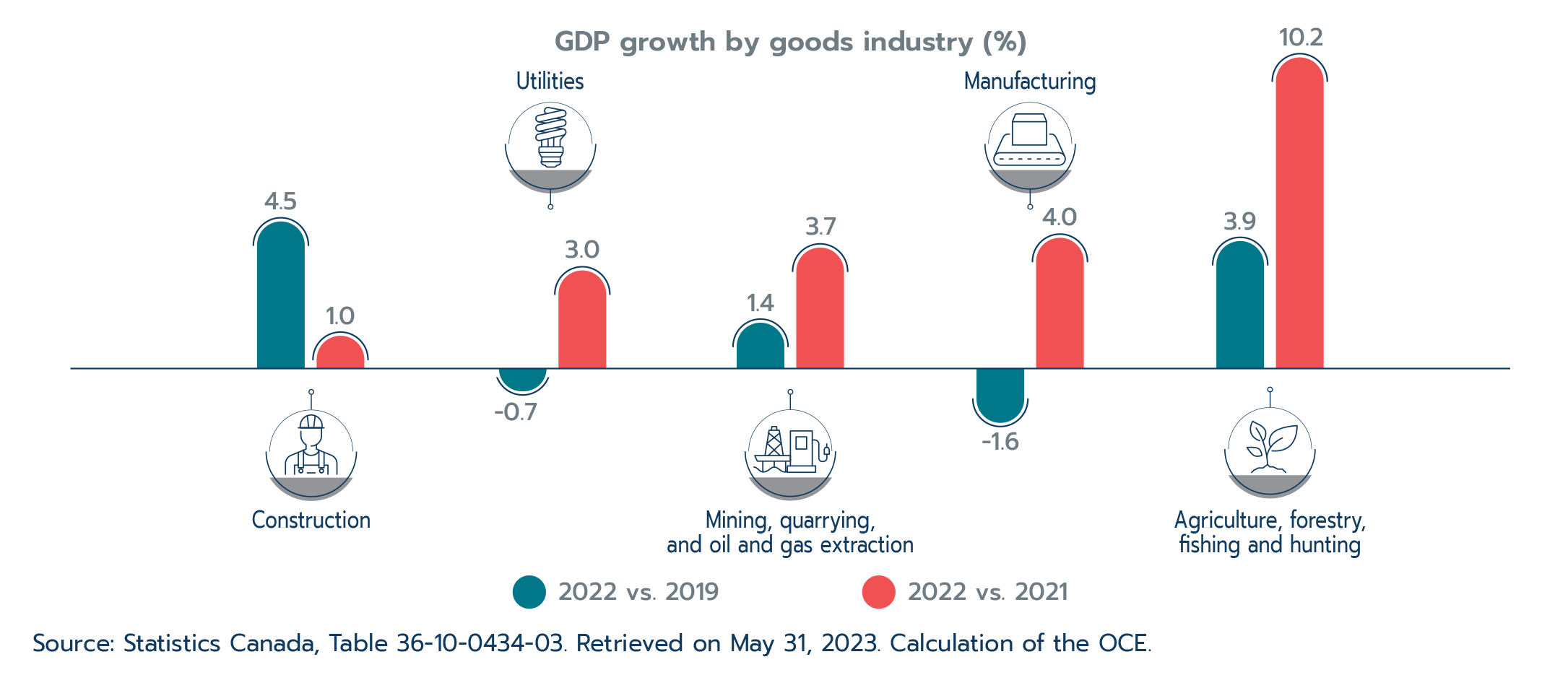

Goods industries advanced by 3.4% in 2022 compared to 2021, led by growth in manufacturing of 4.0%. Supply-chain challenges brought on by the pandemic and semi-conductor shortages moderated in 2022, helping to start a recovery in motor vehicle and parts manufacturing. Despite another year of growth, manufacturing remains below its pre-pandemic level (Figure 1.4).

Favourable weather throughout the year boosted crop production and led to significant growth in agriculture, forestry, fishing, and hunting, helping Canada contribute to filling the gap in global food supplies caused by Russia’s invasion. Mining, quarrying, and oil and gas extraction also posted significant growth in 2022, driven in part by the increase in prices and demand caused by the war in Ukraine. Agriculture, forestry, fishing and hunting, and mining, oil and gas each surpassed their pre-pandemic levels.

Figure 1.4: All goods sectors expanded in 2022, but manufacturing and utilities have yet to recover to their pre-pandemic levels

Text version

GDP growth by goods industry (% change for the economic recovery, 2022 compared to 2019, and % change for 2022 compared to 2021)

| 2022 vs. 2019 | 2022 vs. 2021 | |

|---|---|---|

| Construction | 4.5% | 1.0% |

| Utilities | -0.7% | 3.0% |

| Mining, quarrying, and oil and gas extraction | 1.4% | 3.7% |

| Manufacturing | -1.6% | 4.0% |

| Agriculture, forestry, fishing and hunting | 3.9% | 10.2% |

Source: Statistics Canada, Table 36-10-0434-03. Retrieved on May 31, 2023. Calculation of the OCE.

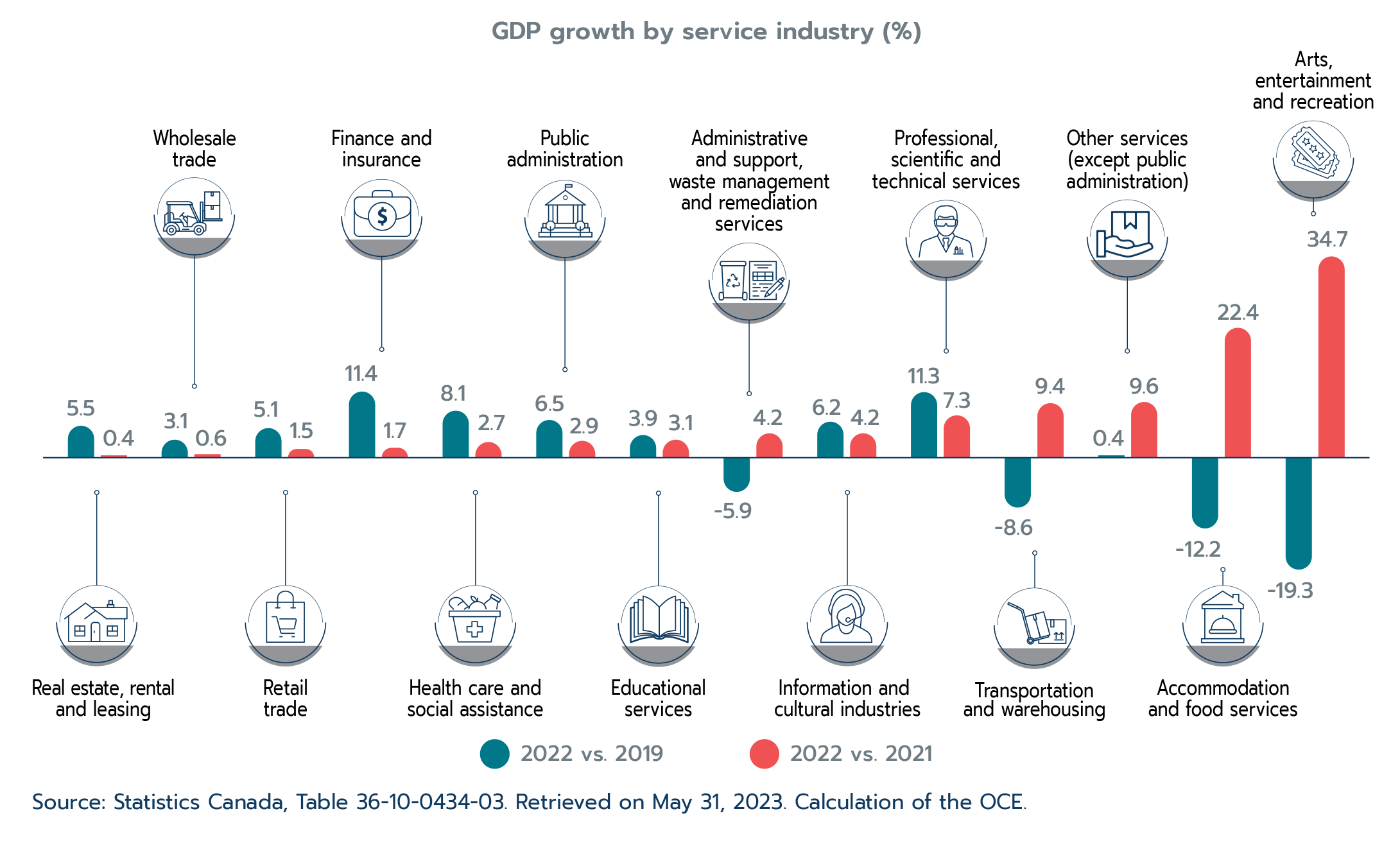

Services industries outperformed goods industries, expanding by 3.7% in 2022. Professional and technical services contributed the most to services industries growth. Meanwhile, public-facing industries hit hardest by the COVID-19 pandemic continued their recovery. Transportation and warehousing expanded by 9.4%, supported by air travel, which benefited from the removal of nearly all COVID-19-related restrictions. Accommodation and food services increased by 22.4% and was the third largest contributor to overall services industries growth in 2022. Despite these solid performances, accommodation and food services, transportation and warehousing, and arts, entertainment and recreation have yet to recover from the effects of the global pandemic (Figure 1.5).

Figure 1.5: Services industries continue their recovery, but several have not reached their pre-pandemic levels

Text version

GDP growth by services industry (% change for the economic recovery, 2022 compared to 2019, and % change for 2022 compared to 2021)

| 2022 vs. 2019 | 2022 vs. 2021 | |

|---|---|---|

| Arts, entertainment and recreation | -19.3% | 34.7% |

| Accommodation and food services | -12.2% | 22.4% |

| Other services (except public administration) | 0.4% | 9.6% |

| Transportation and warehousing | -8.6% | 9.4% |

| Professional, scientific and technical services | 11.3% | 7.3% |

| Information and cultural industries | 6.2% | 4.2% |

| Administrative and support, waste management and remediation services | -5.9% | 4.2% |

| Educational services | 3.9% | 3.1% |

| Public administration | 6.5% | 2.9% |

| Health care and social assistance | 8.1% | 2.7% |

| Finance and insurance | 11.4% | 1.7% |

| Retail trade | 5.1% | 1.5% |

| Wholesale trade | 3.1% | 0.6% |

| Real estate and rental and leasing | 5.5% | 0.4% |

Source: Statistics Canada, Table 36-10-0434-03. Retrieved on May 31, 2023. Calculation of the OCE.

The labour market

After an impressively fast turnaround from the initial shock of the COVID-19 pandemic, the Canadian labour market continued to sprint forward. Indeed, 2022 marked one of the strongest years for the labour market on record. Employment expanded by over 750,000 jobs in 2022. The unemployment rate reached a record low of 4.9% in June of 2022 and averaged 5.3% for the year. Moreover, Canada’s labour force participation rate (i.e., the number of working-age individuals working or looking for work) stayed healthy throughout the year. This suggests that low unemployment was not due to workers dropping out of the labour market. Finally, there was a record-setting million job vacancies (i.e., unmet demand for labour) across the country in May of 2022. While job vacancies came down from this peak, they remained historically high through 2022.

This record strength supported consumer spending and economic activity throughout the year. However, even with this degree of labour market tightness, there were some signs that interest rate increases started to take hold in 2022. In the second half of the year, employment gains slowed, and interest-rate-sensitive sectors saw weaker employment growth. The expectation is for the labour market to cool in 2023 as the effects of higher interest rates fully materialize.

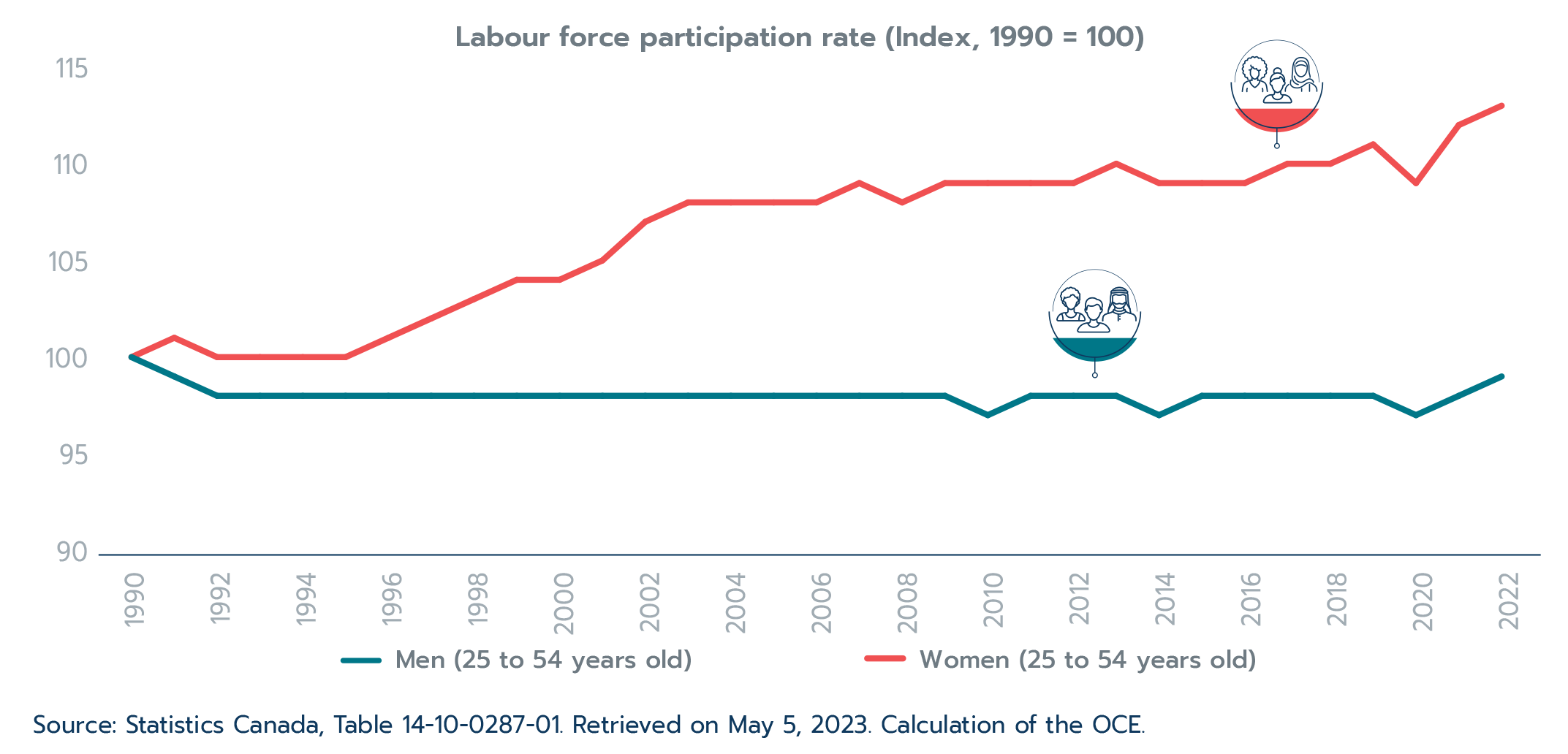

Box 1.1: Women make quick U-turn after initial pandemic-driven job loss

After hitting record unemployment in the wake of the COVID-19 pandemic, the Canadian labour market recovered to the point of record tightness in 2022. Women were a big part of this recovery. The initial shock of the COVID-19 pandemic affected female workers to a much larger extent than their male counterparts.Footnote 1 Several factors drove the contraction in female employment, including the fact that women were disproportionately employed in sectors impacted by COVID-19-related restrictions on in-person services and because of childcare challenges that arose during the pandemic.

However, women were keen to get back to work. Female labour force participation rebounded at a faster rate than for men – the labour force participation rate of core-working-age women (i.e., women 25 to 54 years old) reached a record high of 85.1% in 2022 (Figure 1.6). Several factors could have driven the strong return of women to the job market. For example, the participation rate of women with young children increased substantially in 2022 compared to 2019, which may have been incentivized by additional childcare supports or greater flexibility of work arrangements. Footnote 2

Figure 1.6: Core-working-age women are participating in the labour market at a historic rate

Text version

Core-working-age women are participating in the labour market at a historic rate

Labour force participation rate (Index, 1990 = 100)

| Year | Men (25 to 54 years old) | Women (25 to 54 years old) |

|---|---|---|

| 1990 | 100 | 100 |

| 1991 | 99 | 101 |

| 1992 | 98 | 100 |

| 1993 | 98 | 100 |

| 1994 | 98 | 100 |

| 1995 | 98 | 100 |

| 1996 | 98 | 101 |

| 1997 | 98 | 102 |

| 1998 | 98 | 103 |

| 1999 | 98 | 104 |

| 2000 | 98 | 104 |

| 2001 | 98 | 105 |

| 2002 | 98 | 107 |

| 2003 | 98 | 108 |

| 2004 | 98 | 108 |

| 2005 | 98 | 108 |

| 2006 | 98 | 108 |

| 2007 | 98 | 109 |

| 2008 | 98 | 108 |

| 2009 | 98 | 109 |

| 2010 | 97 | 109 |

| 2011 | 98 | 109 |

| 2012 | 98 | 109 |

| 2013 | 98 | 110 |

| 2014 | 97 | 109 |

| 2015 | 98 | 109 |

| 2016 | 98 | 109 |

| 2017 | 98 | 110 |

| 2018 | 98 | 110 |

| 2019 | 98 | 111 |

| 2020 | 97 | 109 |

| 2021 | 98 | 112 |

| 2022 | 99 | 113 |

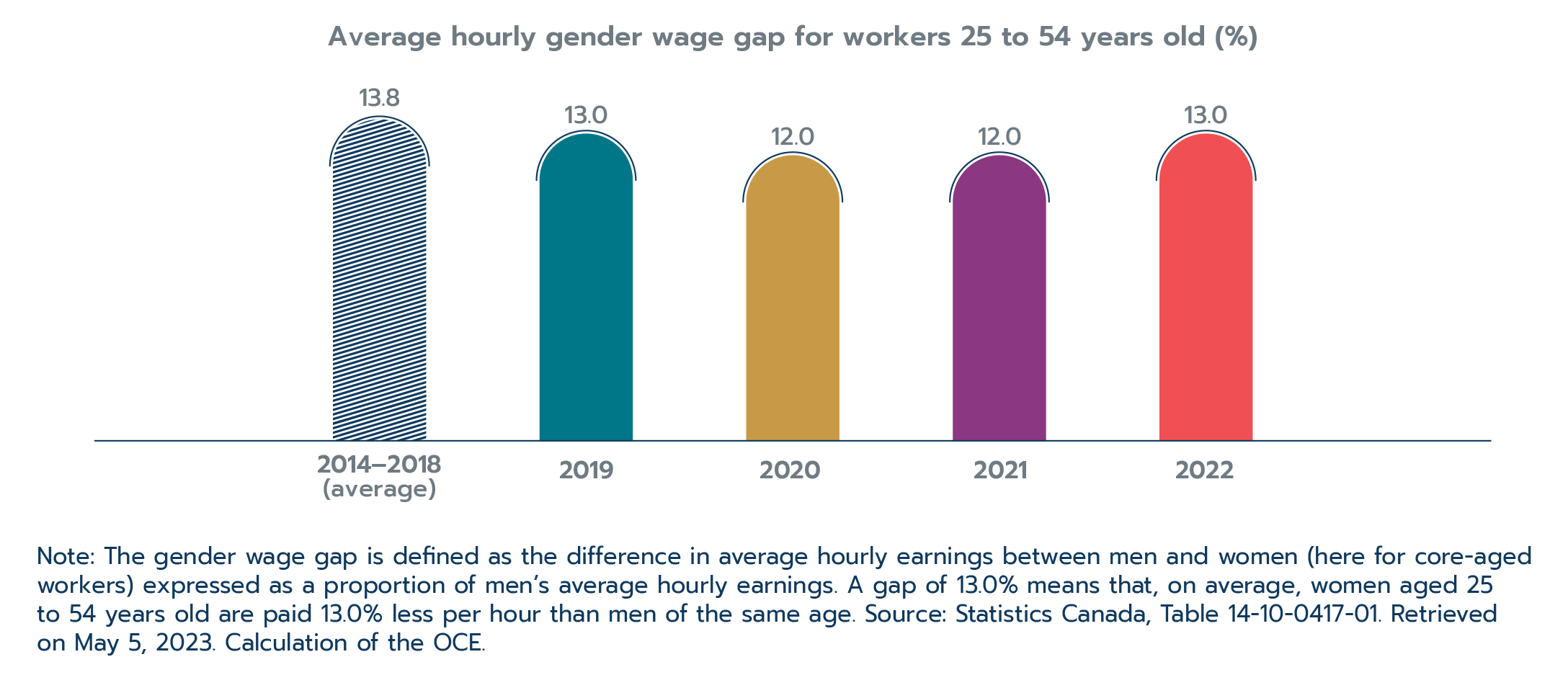

In addition, women shifted to higher-paying jobs as they returned to work. They moved from high-contact jobs, such as those in hospitality, to low-contact jobs, such as those in finance and professional services, which also tend to offer higher wages.Footnote 3 While this shift contributed to an estimated $9-billion advance in women’s wage income, men saw an even greater wage improvement, and the gender wage gap did not narrow over this period (Figure 1.7).Footnote 3 Unfortunately, one explanation of this earnings gap could be that fewer women are in senior management positions.Footnote 3

In sum, women made positive gains during the past several years, but several gender imbalances in the labour market persist.

Figure 1.7: The gender wage gap has not improved compared to 2019 despite changes in female labour market participation and occupational shifts

Text version

The gender wage gap has not improved compared to 2019 despite changes in female labour market participation and occupational shifts

| Year | Average hourly gender wage gap for workers 25 to 54 years old (%) |

|---|---|

| 2014–2018 | 13.8 |

| 2019 | 13.0 |

| 2020 | 12.0 |

| 2021 | 12.0 |

| 2022 | 13.0 |

Note: The gender wage gap is defined as the difference in average hourly earnings between men and women (here for core-aged workers) expressed as a proportion of men’s average hourly earnings. A gap of 13.0% means that, on average, women aged 25 to 54 years old are paid 13.0% less per hour than men of the same age. Source: Statistics Canada, Table 14-10-0417-01. Retrieved on May 5, 2023. Calculation of the OCE.

1.4 Highlights of Canada’s trade performance

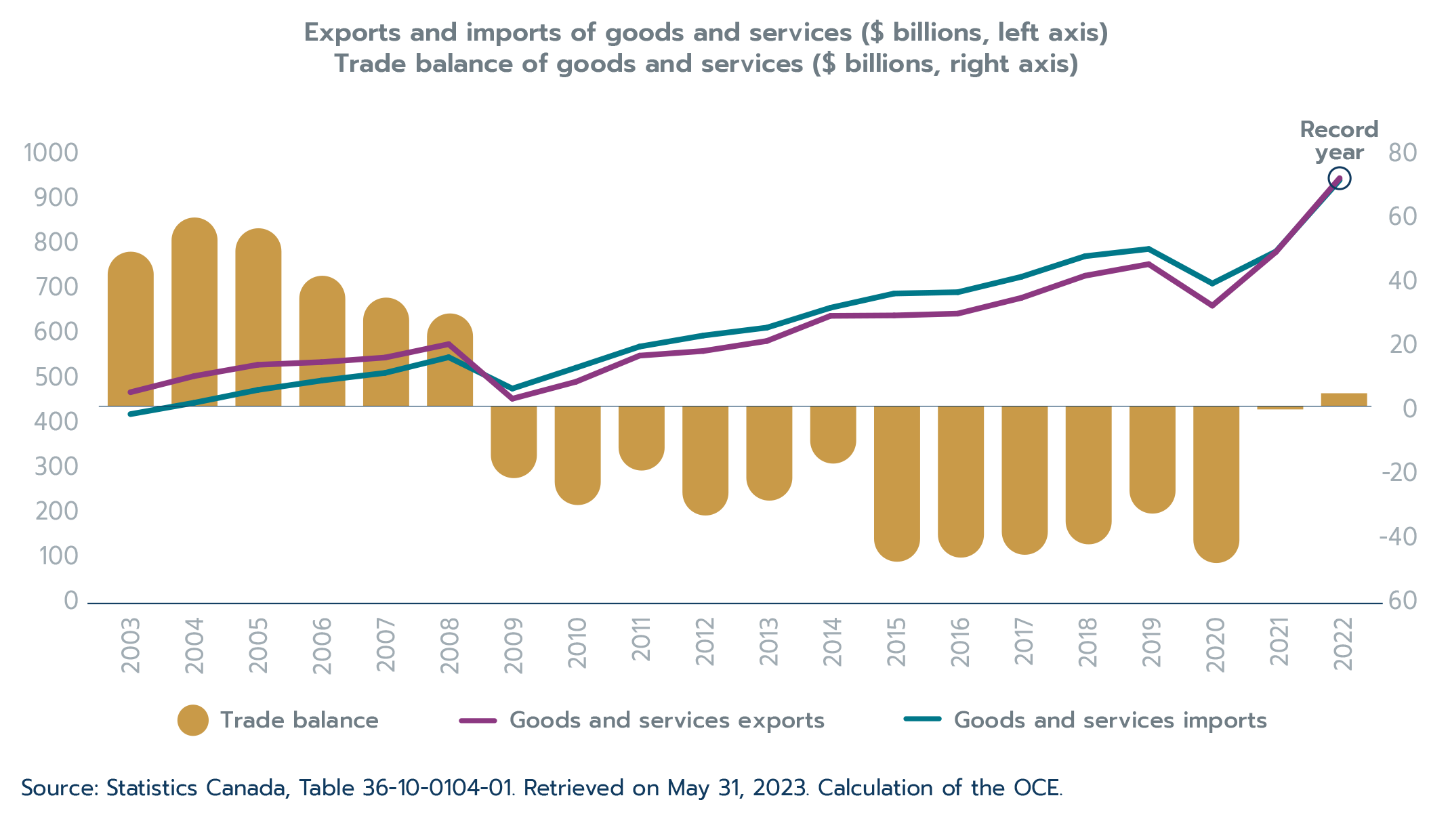

Canada’s international trade posted new records again in 2022. Increasing by 21.2% during the year, goods and services exports reached a record $940.4 billion (Figure 1.8). Goods and services imports also marked new highs, advancing by 20.5% to $936.2 billion in 2022. With exports progressing faster than imports, Canada posted a goods and services trade surplus amounting to $4.1 billion in 2022. Moreover, Canada’s trade-to-GDP ratio was 67.4% in 2022 – the highest level in sixteen years.

Strength in goods prices, particularly for resource exports, and a recovery in services exports and imports drove growth in Canada’s international trade during 2022. This section describes the year’s trends in goods and services trade on a balance-of-payments basis. See the Office of the Chief Economist (2023b) for a review of Canada’s goods trade in 2022 on a customs basis.

Figure 1.8: Canada’s goods and services trade reached new records in 2022

Text version

Canada’s goods and services trade reached new records in 2022

$ Billions (current dollars)

| Goods and services exports | Goods and services imports | Goods and services trade balance | |

|---|---|---|---|

| 2003 | 462.6 | 413.7 | 48.8 |

| 2004 | 498.6 | 439.0 | 59.6 |

| 2005 | 523.9 | 467.7 | 56.2 |

| 2006 | 529.8 | 488.6 | 41.2 |

| 2007 | 540.0 | 505.7 | 34.3 |

| 2008 | 569.9 | 540.7 | 29.3 |

| 2009 | 448.1 | 470.7 | -22.7 |

| 2010 | 485.9 | 517.2 | -31.2 |

| 2011 | 544.3 | 564.5 | -20.3 |

| 2012 | 554.6 | 589.1 | -34.5 |

| 2013 | 577.0 | 606.8 | -29.8 |

| 2014 | 633.1 | 651.2 | -18.1 |

| 2015 | 634.0 | 683.0 | -49.1 |

| 2016 | 638.1 | 685.9 | -47.8 |

| 2017 | 673.3 | 720.3 | -46.9 |

| 2018 | 722.7 | 766.3 | -43.6 |

| 2019 | 748.5 | 782.4 | -33.9 |

| 2020 | 655.9 | 705.4 | -49.5 |

| 2021 | 775.8 | 776.9 | -1.0 |

| 2022 | 940.4 | 936.2 | 4.1 |

Source: Statistics Canada, Table 36-10-0104-01. Retrieved on May 31, 2023. Calculation of the OCE.

Goods trade

Goods exports growth dominated by resource products

Resource exports dominated growth in Canadian goods exports in 2022. Canada’s goods exports increased by 22.4% that year and resource exports accounted for over three-quarters of this growth. Resource exports (28.9%) advanced more than twice as fast as non-resource exports (12.8%) despite both categories of goods showing strength in 2022. Commodity price increases (see Box 1.3), driven by Russia’s invasion of Ukraine, and favourable weather that resulted in high crop yields supported Canada’s resource export growth.

Canada’s goods exports increased by $142.8 billion in 2022. Exports increased across all 11 major goods product categories, with growth fastest in energy (57.0%), metal ores and non-metallic minerals (28.1%), and industrial machinery and equipment (19.1%) (Table 1.1). The war in Ukraine particularly affected oil prices as fears over Europe’s energy supplies mounted. The price of a barrel of crude oil peaked at roughly US$122.7 in June 2022-estimated using the Europe Brent spot price. For the full year, a barrel of crude averaged US$100.9, compared to US$70.9 in 2021. The price of Western Canada Select obtained by many Canadian oil producers followed a similar trend. Energy products alone accounted for over half of Canada’s goods export growth in 2022. Finally, despite recording slower-than-average growth, consumer goods, motor vehicles and parts, and metal and non-metallic mineral products, all posted substantial gains in export values in 2022.

Box 1.2: Goods prices drive export growth for the second consecutive year

Canada’s goods exports reached record levels in 2021 and again in 2022. However, elevated prices drove these records. In 2022, the value of goods exports advanced by roughly 22.5%, with prices increasing by 19.1% and quantities (volumes) gaining 2.7%. Goods export volumes are still modestly below their 2019 pre-pandemic levels, while prices have substantially increased (Figure 1.9).Footnote 1 Footnote 2

In 2022, prices advanced across most major export product categories, with energy product prices increasing notably faster. Export prices for farm and fishing products and for basic chemical products also increased substantially. Russia’s invasion of Ukraine partially drove price increases in energy and other resource product exports as fears around their supply mounted (see Box 1.3). However, record levels of inflation globally also contributed to the widespread increase in Canada’s goods export prices. Export prices were higher in 2022 compared to 2019 across all major goods categories. Meanwhile, export volumes in 2022 were higher in only 3 of 11 product categories compared to their pre-pandemic levels; volumes were higher for energy products, metal ores and non-metallic minerals, forestry products, and consumer goods.

Driven by the product mix of exports to Canada’s trading partners, the role of price and quantity growth differs for each of Canada’s export destinations. For example, prices accounted for the majority of the increase in the value of goods exported to the United States in 2022, but volumes increased too. Meanwhile, export price increases accounted for the entire gain in the value of Canada’s goods exports to China, as goods export quantities decreased significantly.

Figure 1.9: Contributions to Canadian goods export growthFootnote 2

Text version

Contributions to Canadian goods export growth

Ln change from 2019

| Date | Value | Prices | Quantities |

|---|---|---|---|

| 2019-01-01 | -0.036 | -0.030 | -0.006 |

| 2019-02-01 | -0.029 | 0.004 | -0.033 |

| 2019-03-01 | 0.013 | 0.024 | -0.012 |

| 2019-04-01 | 0.023 | 0.030 | -0.008 |

| 2019-05-01 | 0.054 | 0.021 | 0.032 |

| 2019-06-01 | 0.004 | -0.010 | 0.014 |

| 2019-07-01 | -0.004 | -0.015 | 0.010 |

| 2019-08-01 | 0.013 | -0.009 | 0.021 |

| 2019-09-01 | 0.000 | -0.003 | 0.002 |

| 2019-10-01 | -0.013 | -0.008 | -0.006 |

| 2019-11-01 | -0.019 | -0.004 | -0.016 |

| 2019-12-01 | -0.009 | -0.011 | 0.001 |

| 2020-01-01 | -0.047 | -0.020 | -0.028 |

| 2020-02-01 | -0.037 | -0.051 | 0.014 |

| 2020-03-01 | -0.123 | -0.090 | -0.033 |

| 2020-04-01 | -0.448 | -0.187 | -0.263 |

| 2020-05-01 | -0.374 | -0.131 | -0.245 |

| 2020-06-01 | -0.190 | -0.061 | -0.128 |

| 2020-07-01 | -0.105 | -0.038 | -0.068 |

| 2020-08-01 | -0.095 | -0.025 | -0.074 |

| 2020-09-01 | -0.083 | -0.032 | -0.052 |

| 2020-10-01 | -0.068 | -0.017 | -0.052 |

| 2020-11-01 | -0.055 | -0.013 | -0.043 |

| 2020-12-01 | -0.043 | 0.002 | -0.046 |

| 2021-01-01 | 0.034 | 0.035 | 0.011 |

| 2021-02-01 | 0.012 | 0.072 | -0.052 |

| 2021-03-01 | 0.004 | 0.068 | -0.054 |

| 2021-04-01 | 0.009 | 0.094 | -0.083 |

| 2021-05-01 | -0.004 | 0.108 | -0.115 |

| 2021-06-01 | 0.071 | 0.139 | -0.076 |

| 2021-07-01 | 0.081 | 0.154 | -0.088 |

| 2021-08-01 | 0.083 | 0.144 | -0.068 |

| 2021-09-01 | 0.060 | 0.164 | -0.109 |

| 2021-10-01 | 0.128 | 0.199 | -0.075 |

| 2021-11-01 | 0.159 | 0.200 | -0.038 |

| 2021-12-01 | 0.138 | 0.174 | -0.034 |

| 2022-01-01 | 0.154 | 0.233 | -0.080 |

| 2022-02-01 | 0.207 | 0.275 | -0.070 |

| 2022-03-01 | 0.261 | 0.313 | -0.053 |

| 2022-04-01 | 0.283 | 0.332 | -0.050 |

| 2022-05-01 | 0.318 | 0.346 | -0.029 |

| 2022-06-01 | 0.333 | 0.349 | -0.017 |

| 2022-07-01 | 0.292 | 0.315 | -0.024 |

| 2022-08-01 | 0.273 | 0.306 | -0.033 |

| 2022-09-01 | 0.288 | 0.307 | -0.020 |

| 2022-10-01 | 0.290 | 0.308 | -0.019 |

| 2022-11-01 | 0.256 | 0.293 | -0.038 |

| 2022-12-01 | 0.257 | 0.285 | -0.029 |

Statistics Canada, Tables 12-10-0128-01 and 12-10-0121-01. Balance of payments basis, seasonally adjusted. Retrieved in May 2023. Calculation of the OCE.

Canada’s goods imports also reached record levels in 2022. Compared to goods exports, however, the contributions from growth in prices and in quantities were more even. In 2022, goods import prices were up 12.4% while quantities (volumes) increased by 6.6%. Canada’s goods import prices and volumes were above their pre-pandemic levels in 2022.

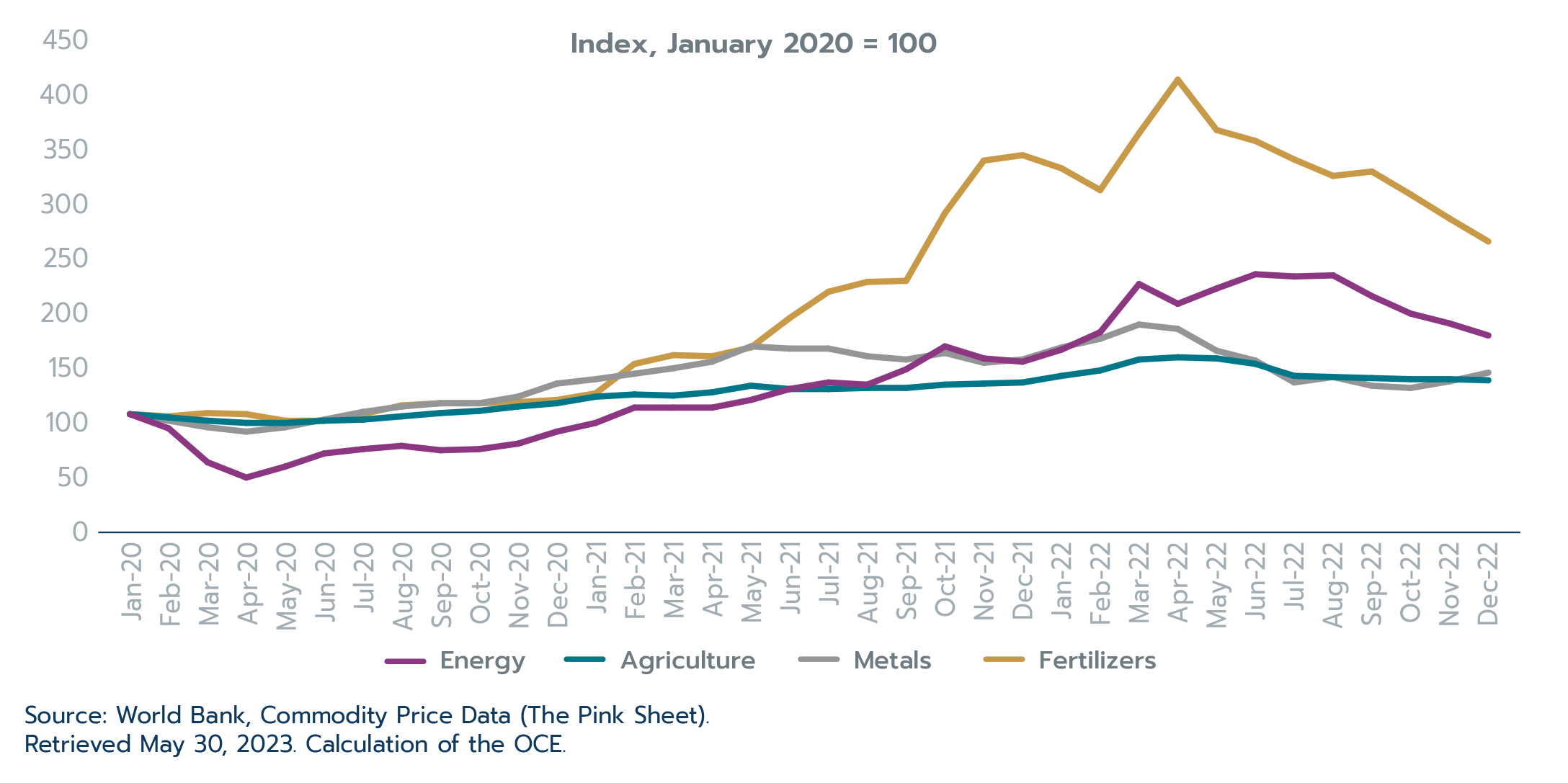

Box 1.3: Commodity prices following Russia’s invasion of Ukraine

Commodity prices have an outsized impact on Canada’s trade performance as commodities account for a large share of our exports. Moreover, commodity prices are set globally and can experience fluctuations given the varied factors that influence the supply and demand for commodities. In 2022, the Russian invasion of Ukraine sent commodity prices into overdrive. Price increases were particularly strong for commodities where the two countries in conflict are large exporters, namely energy products, fertilizers, grains, and metals.Footnote 1

As a major exporter of many affected products, Canada’s monthly export values surged in 2022, especially in the first half of the year. Meanwhile, consumer countries were negatively impacted, for example emerging and developing economies that historically relied on Russia and Ukraine for food supplies. However, prices for many commodities retreated in the second half of 2022 (Figure 1.10). While overall commodity prices remain elevated by historical standards, prices for key products such as energy, metals, agricultural products and fertilizers all fell below pre-invasion levels by the end of the year.

Commodity price fluctuations also have important implications for exchange rates. Commodity exporting countries like Canada saw their currencies appreciate at the beginning of the year while those of importing countries, including Europe and Japan, witnessed exchange rate depreciations. The U.S. dollar strengthened both due to its traditional role as a safe haven in times of uncertainty, and to the fact that it was further supported as that country transitioned to an important energy supplier.

The impact of commodity prices on international trade and exchange rates highlights the interconnectedness of global markets. As a major exporter of commodities, Canada is particularly sensitive to their price fluctuations. Looking ahead, tighter markets in the aftermath of Russia’s invasion mean that commodity prices are likely to remain volatile in the near-term. Monitoring movements of commodity prices and understanding their implications for trade is crucial for navigating the challenges and opportunities of the global economic landscape.

Figure 1.10: Monthly commodity price indices, January 2020 to December 2022

Text version

Monthly commodity price indices, January 2020 to December 2022

Index, January 2020 = 100

| Energy | Agriculture | Metals | Fertilizers | |

|---|---|---|---|---|

| Jan-20 | 100 | 100 | 100 | 100 |

| Feb-20 | 87 | 97 | 94 | 98 |

| Mar-20 | 56 | 94 | 88 | 101 |

| Apr-20 | 42 | 92 | 84 | 100 |

| May-20 | 52 | 92 | 88 | 94 |

| Jun-20 | 64 | 94 | 95 | 94 |

| Jul-20 | 68 | 95 | 102 | 100 |

| Aug-20 | 71 | 98 | 107 | 108 |

| Sep-20 | 67 | 101 | 110 | 110 |

| Oct-20 | 68 | 103 | 110 | 110 |

| Nov-20 | 73 | 107 | 116 | 111 |

| Dec-20 | 84 | 110 | 128 | 113 |

| Jan-21 | 92 | 116 | 132 | 119 |

| Feb-21 | 106 | 118 | 137 | 146 |

| Mar-21 | 106 | 117 | 142 | 154 |

| Apr-21 | 106 | 120 | 148 | 153 |

| May-21 | 113 | 126 | 162 | 161 |

| Jun-21 | 123 | 123 | 160 | 188 |

| Jul-21 | 129 | 123 | 160 | 212 |

| Aug-21 | 127 | 124 | 153 | 221 |

| Sep-21 | 141 | 124 | 150 | 222 |

| Oct-21 | 162 | 127 | 156 | 284 |

| Nov-21 | 151 | 128 | 147 | 332 |

| Dec-21 | 148 | 129 | 150 | 337 |

| Jan-22 | 159 | 135 | 161 | 325 |

| Feb-22 | 175 | 140 | 169 | 305 |

| Mar-22 | 219 | 150 | 182 | 357 |

| Apr-22 | 201 | 152 | 178 | 406 |

| May-22 | 215 | 151 | 158 | 360 |

| Jun-22 | 228 | 146 | 149 | 350 |

| Jul-22 | 226 | 135 | 129 | 333 |

| Aug-22 | 227 | 134 | 134 | 318 |

| Sep-22 | 208 | 133 | 126 | 322 |

| Oct-22 | 192 | 132 | 124 | 301 |

| Nov-22 | 183 | 132 | 130 | 279 |

| Dec-22 | 172 | 131 | 138 | 258 |

Source: World Bank, Commodity Price Data (The Pink Sheet). Retrieved May 30, 2023. Calculation of the OCE.

On the imports side, resources played a less dominant role. Resources account for only about a third of Canada’s goods imports; as such, despite growing faster than non-resource imports (17.7%), resource imports (25.2%) accounted for just over 40% of Canada’s goods import expansion in 2022. Imports growth was much more widespread, with all 11 major product categories rising, and imports of 6 of 11 major product categories gaining over $10 billion each. Overall, goods imports expanded by $125.6 billion. Consumer goods, motor vehicles and parts, and energy products were the largest contributors to the increase in goods imports in 2022. The waning of supply chain issues and the global semiconductor shortage that began in 2021 supported the 20.7% growth in motor vehicles and parts imports.

Table 1.1: Value of Canada’s goods trade by product sector

| 2022 ($ billions) | 2022 vs. 2021 ($ change, billions) | 2022 vs. 2021 (% change) | |

|---|---|---|---|

| Goods exports | |||

| Total | 779.2 | 142.8 | 22.4 |

| Farm, fishing and intermediate food products | 54.5 | 6.9 | 14.6 |

| Energy products | 211.8 | 76.9 | 57.0 |

| Metal ores and non-metallic minerals | 32.9 | 7.2 | 28.1 |

| Metal and non-metallic mineral products | 85.6 | 9.0 | 11.7 |

| Basic and industrial chemical, plastic and rubber products | 44.6 | 5.7 | 14.7 |

| Forestry products, and building and packaging materials | 58.7 | 3.8 | 7.0 |

| Industrial machinery, equipment and parts | 45.2 | 7.2 | 19.1 |

| Electronic and electrical equipment and parts | 31.8 | 4.8 | 17.8 |

| Motor vehicles and parts | 81.0 | 9.0 | 12.5 |

| Aircraft and other transportation equipment and parts | 24.6 | 0.4 | 1.9 |

| Consumer goods | 88.6 | 9.4 | 11.8 |

| Goods imports | |||

| Total | 757.3 | 125.6 | 19.9 |

| Farm, fishing and intermediate food products | 27.9 | 4.1 | 17.4 |

| Energy products | 51.5 | 19.3 | 60.2 |

| Metal ores and non-metallic minerals | 19.3 | 3.9 | 25.2 |

| Metal and non-metallic mineral products | 64.1 | 5.4 | 9.1 |

| Basic and industrial chemical, plastic and rubber products | 67.1 | 15.3 | 29.5 |

| Forestry products, and building and packaging materials | 35.7 | 5.4 | 18.0 |

| Industrial machinery, equipment and parts | 84.6 | 15.8 | 22.9 |

| Electronic and electrical equipment and parts | 84.6 | 10.4 | 14.1 |

| Motor vehicles and parts | 114.8 | 19.7 | 20.7 |

| Aircraft and other transportation equipment and parts | 23.8 | 3.9 | 19.7 |

| Consumer goods | 156.3 | 19.9 | 14.6 |

Source: Statistics Canada, Table 12-10-0122-01. Retrieved on May 31, 2023. Calculation of the OCE.

U.S. economic strength drives growth in Canadian goods exports, while exports to trading partners in non-China Asia and Europe also expand

Total goods exports to Canada’s partners increased by approximately $142.8 billion in 2022, supported by a $118.5 billion increase in exports to the United States (Table 1.2). Growth in goods exports to that country (24.9%) outpaced overall export growth (22.4%). Outside the United States, Japan (+$3.6 billion), India (+$2.4 billion), and South Korea (+$2.4 billion) were the largest contributors to goods export growth. While Brazil falls outside Canada’s top 10 export markets, exports to that country grew rapidly in 2022, expanding by 76.8% as prices for fertilizers and energy rose. Meanwhile, periodic lockdowns linked to the COVID-19 pandemic and weakness in its property market resulted in significantly below-average growth for Canadian exports to China (2.2%), which is Canada’s second-largest goods export market.

The United States also led growth in Canadian goods imports, albeit to a lesser extent than exports. Canada’s goods imports from all countries increased by $125.6 billion in 2022. Imports from all countries (19.9%) and from the United States (20.0%) expanded at a similar pace. After the United States, China (+$12.5 billion, led by large gains in electrical machinery and equipment, and industrial machinery) was the largest contributor to goods import growth, followed by our CUSMA partner, Mexico (+$4.6 billion, predominantly vehicles and vehicle parts, and electrical machinery and equipment). Growth in imports from both countries was marginally faster than growth in imports overall. Growth in imports from the EU (20.9%), South Korea (25.9%), and India (41.1%) also outpaced average import growth and contributed substantially to Canada’s new goods imports record.

Table 1.2: Canada’s goods trade with top 10 trading partners

| 2022 ($ billions) | 2022 vs. 2021 ($ change, billions) | 2022 vs. 2021 (% change) | |

|---|---|---|---|

| Goods exports | |||

| Total, all countries | 779.2 | 142.8 | 22.4 |

| United States | 595.1 | 118.5 | 24.9 |

| China | 29.2 | 0.6 | 2.2 |

| United Kingdom | 19.9 | 1.7 | 9.3 |

| Japan | 18.2 | 3.6 | 24.3 |

| Mexico | 9.9 | 1.0 | 11.4 |

| South Korea | 8.8 | 2.4 | 36.9 |

| Germany | 7.6 | 0.6 | 8.3 |

| Netherlands | 6.6 | 1.7 | 35.1 |

| India | 5.4 | 2.4 | 78.8 |

| Belgium | 4.9 | 1.0 | 24.1 |

| All other countries | 73.6 | 9.4 | 14.7 |

| Goods imports | |||

| Total, all countries | 757.3 | 125.6 | 19.9 |

| United States | 471.4 | 78.5 | 20.0 |

| China | 69.6 | 12.5 | 21.8 |

| Mexico | 24.1 | 4.6 | 23.4 |

| Germany | 18.7 | 3.0 | 18.8 |

| Japan | 12.0 | 0.8 | 6.9 |

| South Korea | 10.9 | 2.2 | 25.9 |

| United Kingdom | 9.9 | -0.1 | -1.1 |

| Italy | 8.9 | 1.4 | 19.3 |

| Switzerland | 7.8 | 0.5 | 6.7 |

| Brazil | 7.5 | 0.8 | 11.7 |

| All other countries | 116.6 | 21.6 | 22.7 |

Source: Statistics Canada, Table 36-10-0023-01. Retrieved on May 30, 2023. Calculation of the OCE.

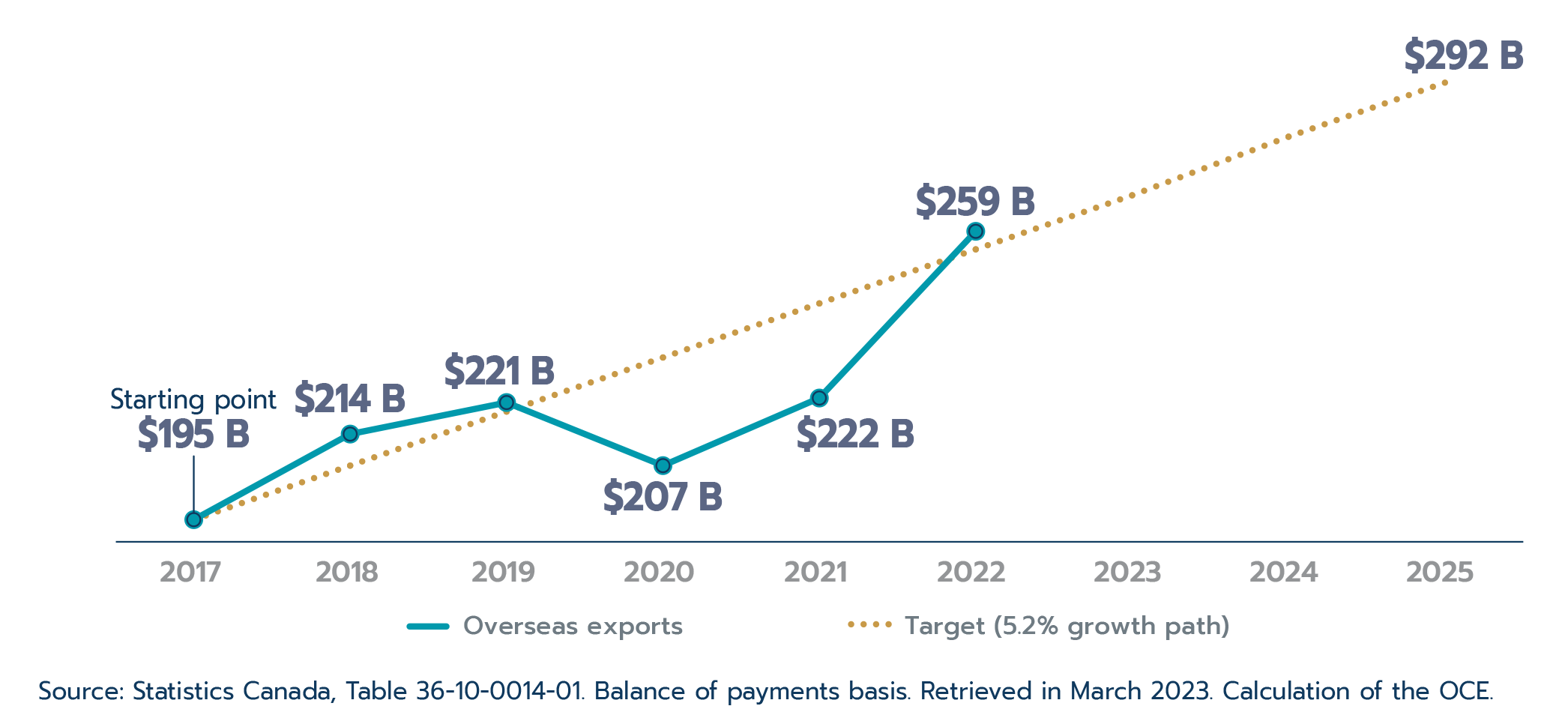

Box 1.4: Canadian goods and services exports back on the path needed to achieve overseas diversification target

The Fall 2018 Economic StatementFootnote 1 set a target of increasing by 50% Canada’s overseas exports by 2025. This target requires that Canadian exports to overseas markets reach $291.8 billion by 2025. If constant growth were to take place, it implies that overseas exports growth would be 5.2% every year, starting in 2017.

After the significant disruption to trade caused by the global pandemic, Canadian overseas exports jumped 16.8% to reach $258.7 billion in 2022. This has not only returned Canadian trade to the path needed to achieve the stated target, but exceeded it (Figure 1.11). As a result, this suggests that Canadian exports to overseas markets would only need to grow by 4.1% annually on average from 2022 on to reach the target in 2025, in the absence of another negative global shock to international trade.

For additional details on the diversification target and Canada’s 2022 performance, see the Office of the Chief Economist’s Growing Canada’s exports to overseas markets by 50% – 2022 Update.

Figure 1.11: Canadian overseas exports rebounded strongly in 2022, getting back on track to reach the growth target

Text version

Contributions to Canadian goods export growth

$ billions

| Overseas exports | Target (5.2% growth path) | |

| 2017 | 195 | 195 |

| 2018 | 214 | 207 |

| 2019 | 221 | 219 |

| 2020 | 207 | 231 |

| 2021 | 222 | 243 |

| 2022 | 259 | 255 |

| 2023 | 267 | |

| 2024 | 280 | |

| 2025 | 292 |

Source: Statistics Canada, Table 36-10-0014-01. Balance of payments basis. Retrieved on May 30, 2023. Calculation of the OCE.

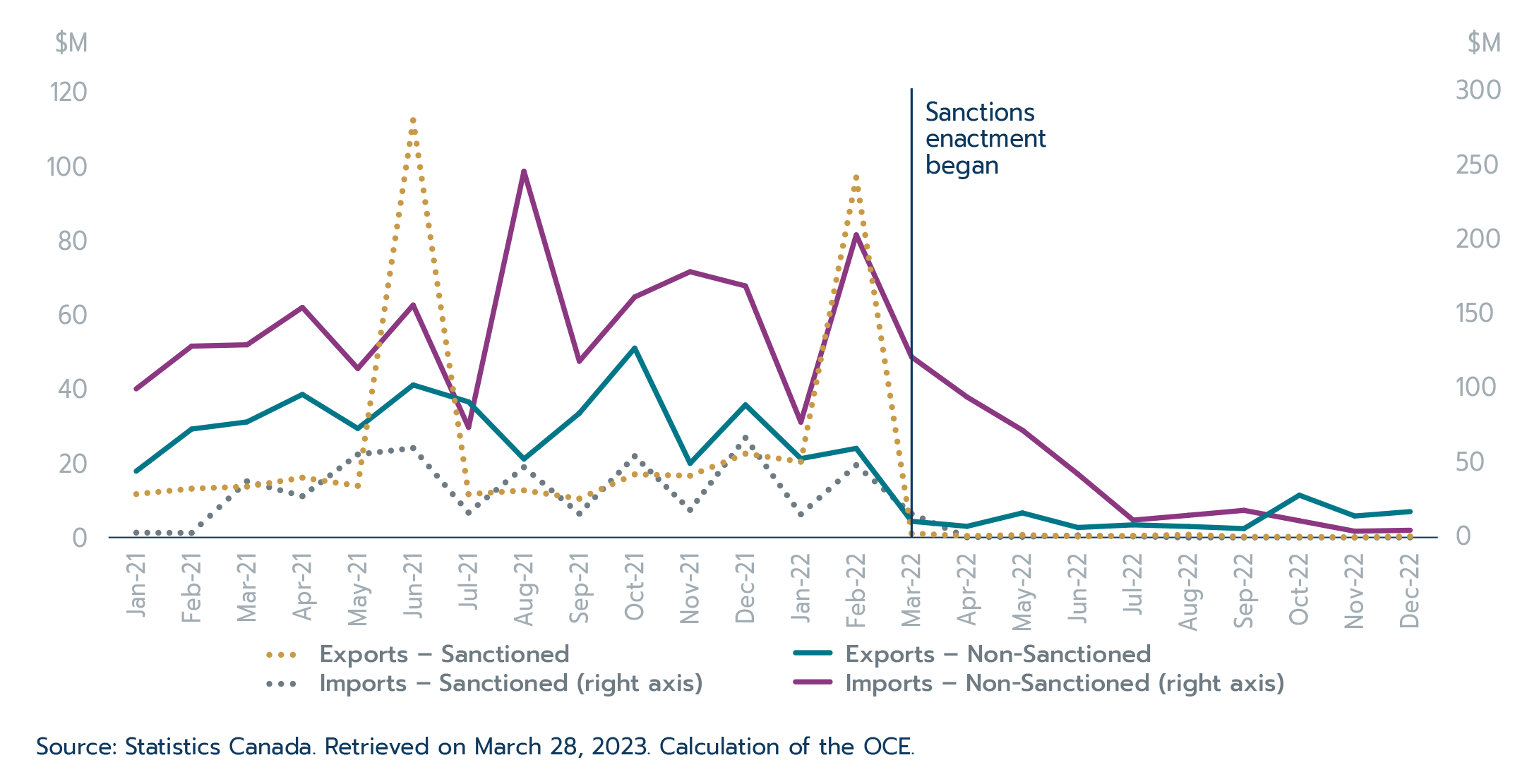

Box 1.5: Canadian merchandise trade with Russia in 2022

Sanctions related to Russia were imposed under the Special Economic Measures Act in order to respond to the gravity of Russia’s violation of the sovereignty and territorial integrity of Ukraine, and grave human rights violations that have been committed in Russia. On March 17, 2014, the Special Economic Measures (Russia) Regulations (“the Regulations”) came into force.

In 2022, the Regulations were amended several times to impose new asset freezes and dealing prohibitions on designated persons listed in Schedule 1, which include both individuals and entities. Furthermore, the 2022 amendments created new prohibitions on exports and imports of certain productsFootnote 1 to and from Russia as a consequence of Russia’s invasion of Ukraine. The prohibited export products include luxury goods, materials used in the production of weapons, advanced goods and technologies, and others. The prohibited import products include petroleum products, luxury goods, gold products, and others. In general, the sanction on these products aimed to limit Russia’s production and ability to raise funds for its war efforts. The majority of these export and import prohibitions were enacted between March and July 2022.

Canadian total merchandise trade with Russia in 2022 reflects the impact of these measures (Figure 1.12). It declined 65.1% in 2022, with exports decreasing 67.2% and imports down 64.5%. Trade for both sanctioned and non-sanctioned products fell significantly. Exports of sanctioned products declined 55.7% in 2022, and were close to zero in the later part of the year. Prior to the sanctions, exports of sanctioned products saw two significant spikes in June 2021 and February 2022; both were the result of higher sales of airplanes and other aircrafts (Harmonized System code 880230 and 880240), a product group that often display spikes in trade value due to the high-value nature of these products and the infrequency of sales. Even though there are still some exports of non-sanctioned products such as vaccines for human medicines and eggs of birds, these too dropped significantly in 2022.

On the import side, sanctioned products declined 79.7% in 2022 as the value of Canada’s imports of these products from Russia essentially fell close to zero in the second half of the year. The slower decline of imports may be due to importers needing to find alternative suppliers or to the lag between the time the orders were made (possibly before February 2022) and the time when the products were shipped and received. Imports of non-sanctioned products were down 60.9% in 2022, but there were still some imports occurring in the latter part of 2022.

Figure 1.12: Canadian merchandise trade with Russia

Text version

Canadian merchandise trade with Russia ($)

| Exports - Sanctioned | Exports - Non Sanctioned | Imports - Sanctioned | Imports - Non-Sanctioned | |

|---|---|---|---|---|

| Jan 2021 | 11,683,791 | 17,860,615 | 3,237,187 | 100,064,080 |

| Feb 2021 | 13,155,912 | 29,198,418 | 3,082,905 | 128,812,765 |

| Mar 2021 | 13,712,626 | 31,117,665 | 37,799,476 | 129,713,216 |

| Apr 2021 | 16,104,360 | 38,519,194 | 27,826,807 | 154,866,478 |

| May 2021 | 13,911,728 | 29,357,684 | 55,880,867 | 113,751,726 |

| Jun 2021 | 112,310,124 | 41,071,834 | 60,182,903 | 156,455,908 |

| Jul 2021 | 11,669,249 | 36,510,684 | 16,764,439 | 74,144,578 |

| Aug 2021 | 12,678,348 | 21,131,469 | 47,310,133 | 246,538,826 |

| Sep 2021 | 10,455,380 | 33,456,493 | 16,087,696 | 118,658,314 |

| Oct 2021 | 17,001,171 | 50,985,269 | 54,705,746 | 161,890,673 |

| Nov 2021 | 16,633,497 | 19,976,640 | 18,591,389 | 178,902,326 |

| Dec 2021 | 22,567,703 | 35,703,953 | 67,046,359 | 169,314,024 |

| Jan 2022 | 20,400,371 | 21,244,695 | 15,639,132 | 77,653,937 |

| Feb 2022 | 96,899,105 | 23,997,181 | 48,665,920 | 203,682,136 |

| Mar 2022 | 1,104,016 | 4,356,268 | 15,953,843 | 121,505,857 |

| Apr 2022 | 393,856 | 3,006,924 | 178,002 | 94,571,703 |

| May 2022 | 675,594 | 6,618,696 | 488,485 | 72,249,927 |

| Jun 2022 | 268,424 | 2,696,619 | 1,368,240 | 42,747,865 |

| Jul 2022 | 446,803 | 3,396,700 | 731,253 | 11,704,631 |

| Aug 2022 | 74,943 | 2,965,971 | 8 | 14,952,074 |

| Sep 2022 | 18,750 | 2,392,305 | 0 | 18,272,643 |

| Oct 2022 | 21,637 | 11,391,861 | 57,526 | 11,269,390 |

| Nov 2022 | 4,982 | 5,789,727 | 92 | 4,231,851 |

| Dec 2022 | 33,912 | 6,965,930 | 0 | 4,868,289 |

Source: Statistics Canada. Retrieved on March 28, 2023. Calculation of the OCE.

Services trade

Services trade recovery led by strength in the still recovering travel services sector

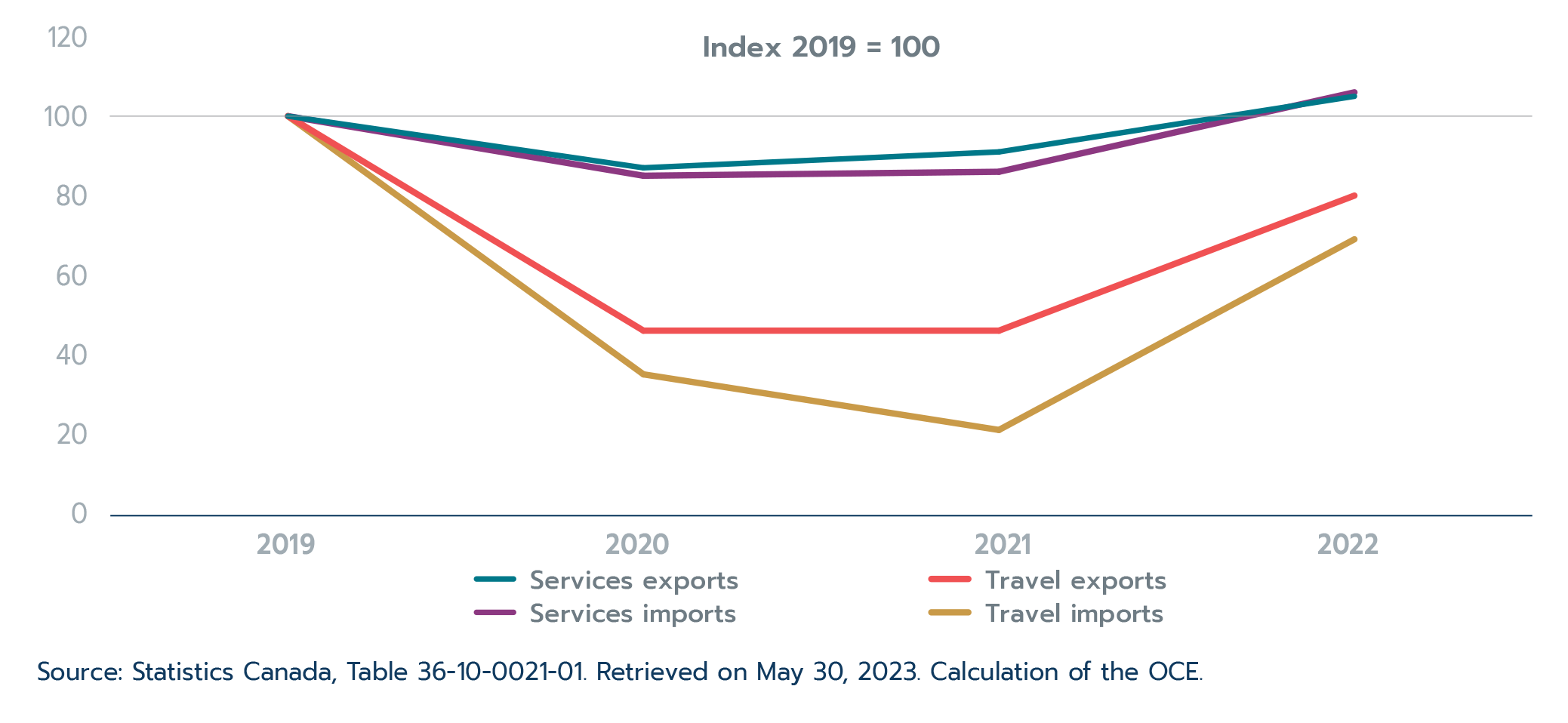

Compared to goods, the global pandemic had longer lasting effects on services trade. Restrictions on travel and in-person gatherings meant that many client-facing sectors suffered greatly during the past several years. With the elimination of Canada’s COVID-19-related restrictions in 2022, services exports and imports surpassed their 2019 levels (Figure 1.13), while goods exports and imports had already done so the year before. Travel services in particular are still in recovery mode, while commercial services were in fact one of the sectors least impacted by the pandemic (even compared to goods) and have seen steady growth over the past two years.

Figure 1.13: Services trade surpasses pre-pandemic levels but travel services are still struggling

Text version

Services trade surpasses pre-pandemic levels but travel services are still struggling

Index 2019 = 100

| 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|

| Services exports | 100 | 87 | 91 | 105 |

| Travel exports | 100 | 46 | 46 | 80 |

| Services imports | 100 | 85 | 86 | 106 |

| Travel imports | 100 | 35 | 21 | 69 |

Source: Statistics Canada, Table 36-10-0021-01. Retrieved on May 30, 2023. Calculation of the OCE.

Canada’s services exports reached new highs in 2022, increasing by 15.6% to $161.2 billion (Table 1.3). Exports across all four major services sectors increased, with travel services driving growth. Travel and transportation services posted strong growth in 2022 as they continued to recover alongside the removal of COVID-19-related restrictions. Travel services exports increased by a robust 74.8% to reach $31.7 billion, accounting for over sixty percent of overall services export growth. Transportation services exports (27.8%), which were also impacted by physical restrictions in place due to COVID-19, also increased faster than services exports overall. Government services exports, which also saw a significant contraction in 2020, expanded by 3.9% in 2022. Meanwhile, commercial services exports, which grew steadily throughout the pandemic, posted modest growth of 3.8% in 2022. The strong 2022 performance helped services exports surpass their pre-pandemic levels.

Overall, services exports were 5.4% above their pre-pandemic levels in 2022, but travel services were still 19.9% below their pre-pandemic levels. The number of travellers entering Canada reflects these trends (see Box 1.6). Government services exports, which account for only about one percent of services exports, also remained below their pre-pandemic levels in 2022.

Table 1.3: Canada’s services trade by sector

| 2022 ($ billions) | 2022 vs. 2021 ($ change, billions) | 2022 vs. 2021 (% change) | |

|---|---|---|---|

| Services exports | |||

| Total, services | 161.2 | 21.7 | 15.6 |

| Travel services | 31.7 | 13.6 | 74.8 |

| Transportation services | 19.0 | 4.1 | 27.8 |

| Commercial services | 109.1 | 4.0 | 3.8 |

| Government services | 1.5 | 0.1 | 3.9 |

| Services imports | |||

| Total, services | 178.9 | 33.8 | 23.3 |

| Travel services | 32.2 | 22.3 | 225.4 |

| Transportation services | 36.1 | 9.1 | 33.9 |

| Commercial services | 108.8 | 2.2 | 2.1 |

| Government services | 1.8 | 0.1 | 4.3 |

Source: Statistics Canada, Table 36-10-0021-01. Retrieved on May 30, 2023. Calculation of the OCE.

Services imports outpaced services exports, growing by 23.3% to reach $178.9 billion in 2022 (Table 1.3). Faster growth in services imports resulted from the still-recovering travel services sector, which accounted for a larger share of the growth in services imports than services exports. Despite the faster growth, services imports and exports displayed similar trends. Travel services imports led growth, increasing to $32.2 billion in 2022, equivalent to over three times their 2021 levels. Travel services imports accounted for about two-thirds of services import growth in 2022. Transportation services imports (+33.9%) also outpaced services import growth overall, while commercial (+2.1%) and government (+4.3%) services imports increased at a slower-than-average pace. Despite the over three-fold increase in travel services imports, they remain 31.3% below their pre-pandemic levels. Meanwhile, services imports as a whole ended 2022 at 6.5% above their 2019 levels.

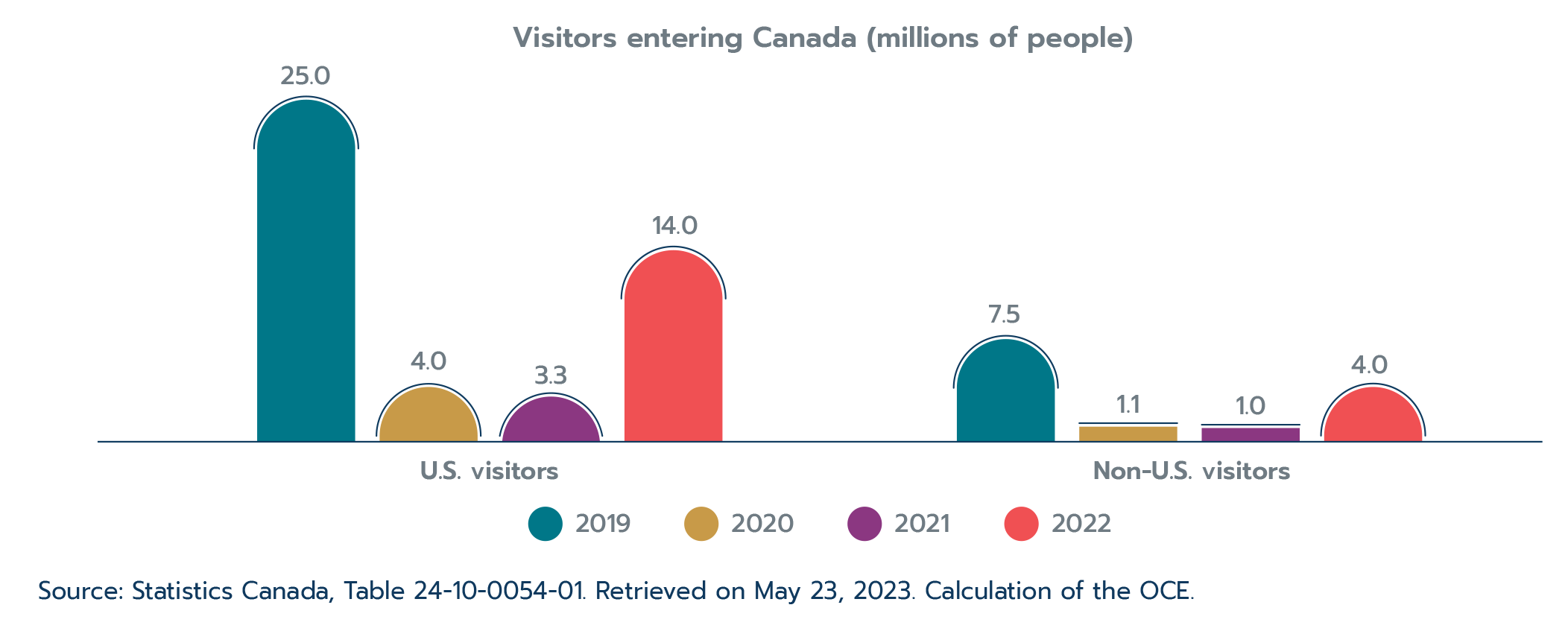

Box 1.6: More Canadians travelled abroad, and visits to Canada increased in 2022, but traveller volumes have yet to reach pre-pandemic levels

Before the pandemic, travel services accounted for 25.9% of Canada’s total services exports – second only to commercial services. However, with the implementation of public health protocols to stop the spread of COVID-19 and the general reluctance of people to travel, travel services trade plummeted; as a result, travel services only accounted for 19.7% of Canada’s total services exports by 2022, remaining 19.9% below their pre-pandemic levels.

Looking at the number of visitors to Canada is another way to view the impact of the pandemic on travel services exports. Over four times as many travellers visited Canada in 2022 compared to the previous year. This significant increase resulted in over 17.9 million visitors entering Canada in 2022. Visits from U.S. travellers accounted for 77.9% of total visits to Canada, outpacing growth in visits from residents of non-U.S. locations.

While the 2022 increase in travellers to Canada was notable, the total number of travellers remains significantly below pre-pandemic levels (Figure 1.14). Over 14.5 million fewer travellers entered Canada in 2022 compared to 2019; visits from U.S. and non-U.S. travellers were roughly 44.0% and 47.0% lower in 2022 than in 2019, respectively. The Canadian economy lost out on the benefits associated with spending by these 14.5 million visitors, impacting many services sectors.

Figure 1.14: Over 14.5 million fewer travellers visited Canada in 2022 than in 2019

Text version

Over 14.5 million fewer travellers visited Canada in 2022 compared to 2019.

Visitors entering Canada (millions of persons)

| 2019 | 2020 | 2021 | 2022 | |

|---|---|---|---|---|

| U.S. visitors | 25.0 | 4.0 | 3.3 | 14.0 |

| Non-U.S. visitors | 7.5 | 1.1 | 1.0 | 4.0 |

Source: Statistics Canada, Table 24-10-0054-01. Retrieved on May 23, 2023. Calculation of the OCE.

Travel services imports followed a similar trend; the number of Canadians travelling abroad was over four times higher in 2022 than in 2021 but remained 43.1% below 2019 levels. Canada dropped all of its COVID-19-related travel restrictions in the fall of 2022, which boosted travel to and from the country in the fourth quarter. The outlook for travel in 2023 is hard to predict as fewer COVID-19 travel restrictions internationally and a gloomier global economic outlook may have opposite effects on the industry’s recovery.

The United States helped support the services trade recovery

Canada’s services exports increased by $21.7 billion in 2022, with services exports to the United States (+$8.9 billion) making the largest contribution, despite posting slower growth than services exports overall (Table 1.4). Services exports to each of Canada’s major trading partners advanced in 2022. The second and third largest contributions to services export growth in 2022 came from China (+$2.0 billion) and India (+$1.2 billion), where services exports expanded faster than the average. Services exports to France, Hong Kong, and Mexico also rose at an above-average pace in 2022. Among Canada’s top 10 services export markets, China (-11.6%), Germany (-10.5%) and Japan (-8.0%) remain below their pre-pandemic levels. Travel and transportation services continue to hold down the services export recovery in these markets while commercial services exports surpassed their pre-pandemic levels in 2021.

Even more than for exports, the United States led Canada’s services import growth in 2022. Services imports increased by $33.8 billion over the year, while imports from that country grew by $19.0 billion. After the United States, services imports from the United Kingdom (+$1.3 billion) and Mexico (+$ 1.1 billion) made the largest contributions to growth in 2022. As with exports, growth in Canada’s services imports was widespread, with imports from all major trading partners rising in 2022. Except for services imports from Mexico and Japan, imports from Canada’s top 10 trading partners in 2022 were above their pre-pandemic levels.

Table 1.4: Canada’s services trade with top 10 trading partners

| 2022 ($ billions) | 2022 vs. 2021 ($ change, billions) | 2022 vs. 2021 (% change) | |

|---|---|---|---|

| Services exports | |||

| Total, all countries | 161.2 | 21.7 | 15.6 |

| United States | 86.6 | 8.9 | 11.5 |

| United Kingdom | 7.7 | 0.9 | 13.7 |

| China | 7.6 | 2.0 | 36.7 |

| India | 6.2 | 1.2 | 25.4 |

| France | 4.7 | 1.0 | 26.2 |

| Germany | 3.2 | 0.1 | 4.0 |

| Hong Kong | 2.5 | 0.5 | 22.6 |

| Switzerland | 2.5 | 0.2 | 10.0 |

| Japan | 2.0 | 0.4 | 23.7 |

| Netherlands | 2.0 | 0.1 | 6.6 |

| All other countries | 36.2 | 6.3 | 21.1 |

| Services imports | |||

| Total, all countries | 178.9 | 33.8 | 23.3 |

| United States | 101.7 | 19.0 | 23.0 |

| United Kingdom | 9.3 | 1.3 | 16.4 |

| Hong Kong | 6.3 | 0.9 | 17.1 |

| China | 4.3 | 0.9 | 26.7 |

| Germany | 4.0 | 0.6 | 18.9 |

| France | 3.6 | 0.8 | 28.0 |

| Singapore | 3.1 | 0.4 | 15.1 |

| Japan | 3.0 | 0.7 | 31.9 |

| India | 2.9 | 0.5 | 19.5 |

| Mexico | 2.6 | 1.1 | 72.5 |

| All other countries | 38.1 | 7.5 | 24.4 |

Source: Statistics Canada, Table 12-10-0157-01. Retrieved on May 30, 2023. Calculation of the OCE.

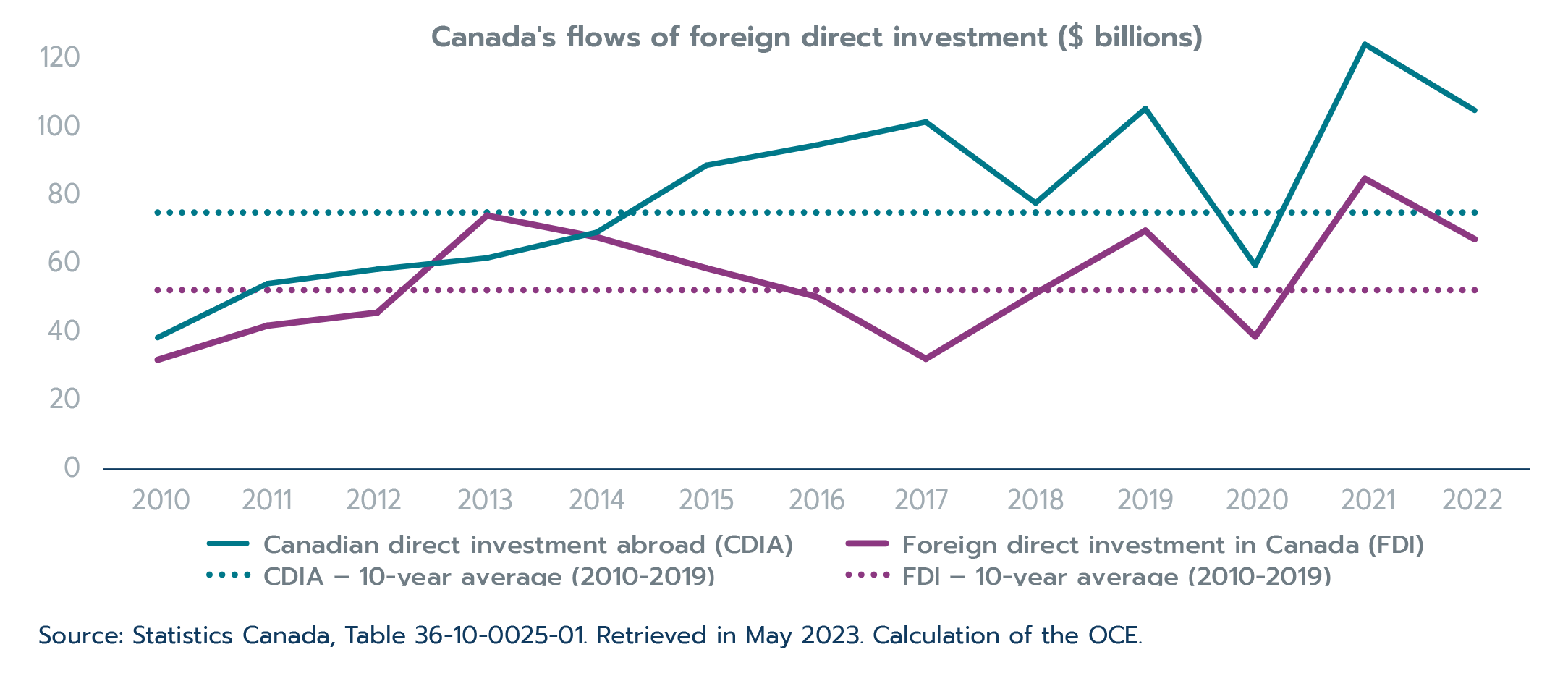

1.5 Canadian foreign direct investment performance

Following significant rebounds in 2021, both Canadian direct investment abroad (CDIA) and foreign direct investment (FDI) flows declined in 2022. Nevertheless, CDIA and FDI flows remained above their average of the pre-pandemic decade (2010‒2019), but below their 2019 levels. More specifically, after rising to a record $121.6 billion in 2021, CDIA flows declined 15.8% to $102.3 billion in 2022, which is still above the $72.4 billion average for 2010‒2019 (Figure 1.15), but below the 2019 pre-pandemic level ($102.8 billion). Similarly, FDI flows decreased 21.5% from a record $82.3 billion in 2021 to $64.6 billion in 2022, still higher than the 2010‒2019 average of $49.8 billion, but below the 2019 pre-pandemic level ($67.1 billion).

The decline in CDIA flows in 2022 was led by mergers and acquisitions (M&As), which fell 57.6% to $27.2 billion, offsetting a quadruple increase in “other flows” Footnote 2 ($13.5 billion) and a 13.4% increase in reinvested earnings Footnote 3 (to a record $61.6 billion). The decrease in FDI flows, on the other hand, was driven largely by a substantial 89.6% drop in “other flows” (to a record low of $2.2 billion), as well as a 7.6% decline in M&As ($19.2 billion). These declines offset a 7.8% increase in reinvested earnings to a record $43.2 billion.

Notably, over the last decade (2013‒2022), reinvested earnings were the largest component of CDIA flows for about half of the years (2013, 2018‒2020 and 2022). In other years, M&As were the largest component. Reinvested earnings were the largest component for FDI flows in nearly every year over the past decade, except for 2014‒2015 and 2020 when M&As dominated.

As shown in Figure 1.15, CDIA flows outpaced FDI flows in 2022, the continuation of a trend observed since 2014.

Figure 1.15: Declines in both Canada’s FDI inflows and outflows in 2022

Text version

Declines in both Canada’s FDI inflows and outflows in 2022

Canada’s flows of foreign direct investment

| Canadian direct investment abroad ($ billions) | Foreign direct investment in Canada ($ billions) | |

|---|---|---|

| 2010 | 35.8 | 29.3 |

| 2011 | 51.6 | 39.3 |

| 2012 | 55.8 | 43.1 |

| 2013 | 59.1 | 71.5 |

| 2014 | 66.6 | 65.2 |

| 2015 | 86.2 | 56.1 |

| 2016 | 92.1 | 47.8 |

| 2017 | 98.9 | 29.6 |

| 2018 | 75.2 | 48.8 |

| 2019 | 102.8 | 67.1 |

| 2020 | 56.9 | 36.1 |

| 2021 | 121.6 | 82.3 |

| 2022 | 102.3 | 64.6 |

| 10-year average | 72.4 | 49.8 |

Source: Statistics Canada, Table 36-10-0025-01, Retrieved in May 2023. Calculation of the OCE.

Overall, global FDI inflows and outflows mostly followed the same pattern as Canadian FDI inflows and outflows, so Canadian trends are largely in line with international trends.

Sectoral composition

The finance and insurance sector represented the highest share of CDIA flows in 2022 at 46.9%, followed by energy and mining at 16.9% and management of companies and enterprises at 16.7%. CDIA from the finance and insurance sector rose 50.6% to $48.0 billion in 2022, the highest since the record $54.3 billion reached in 2015. Other notable gains were in energy and mining, which nearly tripled to $17.3 billion, and manufacturing, which also almost tripled to $6.5 billion. The trade and transportation sector, which accounted for almost half of CDIA flows in 2021, experienced a massive 94.2% drop in 2022 to $3.4 billion.

With respect to FDI flows, the management of companies and enterprises Footnote 4 sector nearly doubled in 2022 to $11.4 billion, the highest level since 2014 and almost double its pre-pandemic level of 2019. The 21.5% decline in FDI flows between 2021 and 2022 was attributed largely to a 73.3% decrease in the “other industries” sector to $3.6 billion. It now represents the lowest sectoral share of FDI flows in 2022 at 5.5%. Other notable declines were in energy and mining (-16.0%), manufacturing (-32.6%), and finance and insurance (-9.8%). Despite these declines, the manufacturing sector continued to account for the largest share of FDI flows in 2022 at 24.0%, followed by energy and mining (21.8%), and trade and transportation (17.8%).

Table 1.5: CDIA and FDI flows by sector (2022)

| Value ($B) | Change from 2021 (%) | Change from 2021 ($B) | |

|---|---|---|---|

| CDIA | |||

| Energy and mining | 17.3 | 198.0 | 11.5 |

| Manufacturing | 6.5 | 181.3 | 4.2 |

| Trade and transportation | 3.4 | -94.2 | -56.2 |

| Finance and insurance | 48.0 | 50.6 | 16.1 |

| Management of companies and enterprises | 17.1 | 23.2 | 3.2 |

| Other industries | 10.0 | 23.3 | 1.9 |

| Total | 102.3 | -15.8 | -19.3 |

| FDI | |||

| Energy and mining | 14.1 | -16.0 | -2.7 |

| Manufacturing | 15.5 | -32.6 | -7.5 |

| Trade and transportation | 11.5 | -3.7 | -0.4 |

| Finance and insurance | 8.5 | -9.8 | -0.9 |

| Management of companies and enterprises | 11.4 | 46.5 | 3.6 |

| Other industries | 3.6 | -73.3 | -9.8 |

| Total | 64.6 | -21.5 | -17.7 |

Source: Statistics Canada, Table 36-10-0026-01. Retrieved in May 2023. Calculation of the OCE.

Geographic composition

The United States continues to be Canada’s top investment partner as the destination of 52.3% ($53.6 billion) of CDIA flows and the source of 41.5% ($26.8 billion) of all FDI inflows in 2022. However, while the United States was the main driver of Canada’s 2021 investment recovery, it also led Canada’s investment decline in 2022. There was a $22.7 billion drop in CDIA flows destined to the United States between 2021 and 2022, and a $9.9 billion loss of FDI inflows from the United States during the same period.

The United Kingdom was the second largest destination of CDIA flows in 2022 with a 5.0% share, followed by Australia (3.9%) and Switzerland (3.6%). CDIA flows to the United Kingdom made a significant recovery in 2022, nearly tripling to $5.2 billion, while CDIA flows to Switzerland grew more than five times to $3.7 billion. Important destinations of CDIA such as France, Luxembourg, and the Netherlands reported decreases of 72.4%, 118.4%, and 485.4%, respectively, with France dropping out of the top 10 in 2022 from fourth place in 2021. In level terms, the drop in FDI outflows in 2022 was led by the United States (-$22.7 billion), Luxembourg (-$5.8 billon), and France (-$3.5 billion).

As for Canada’s FDI sources, the United States accounted for 41.5% of FDI inflows in 2022, followed by the Netherlands and Luxembourg, which together represented 32.3% of inflows. Other important FDI sources in 2022 were Australia (7.7%), the United Kingdom (6.5%), Brazil (3.2%), and France (3.1%). Among these countries, gains were reported by the Netherlands (+19.5%), Luxembourg (+90.9%) and Australia (+1,896.4%), while the United States (-26.9%), the United Kingdom (-59.8%), Brazil (-10.9%), and France (-36.8%) posted losses. In level terms, the decline in FDI inflows in 2022 was driven by the United States (-$9.8 billion), the Cayman Islands (-$7.3 billion) and the United Kingdom (-$6.2 billion).

In the last decade (2013‒2022), the average share of FDI inflows from the United States was 47.6%. Since 2018, the share value of that country has been below the 10-year average fluctuating between 35.6% and 44.6%. For FDI outflows, the 10-year average for flows to the United States was 64.1%. Since 2019, the share value remained below the average, with the exception of 2020 when it reached 71.1%.

Table 1.6: CDIA and FDI flows (2022) – Top 10 countries

| Value ($B) | Change from 2021 (%) | Change from 2021 ($B) | |

|---|---|---|---|

| CDIA destinations | |||

| United States | 53.6 | -29.8 | -22.7 |

| United Kingdom | 5.2 | 172.2 | 3.3 |

| Australia | 4.0 | -23.3 | -1.2 |

| Switzerland | 3.7 | 421.5 | 3.0 |

| Brazil | 3.4 | 8.3 | 0.2 |

| Barbados | 3.1 | -244.3 | 5.3 |

| Cayman Islands | 3.0 | 387.9 | 2.4 |

| Netherlands | 2.1 | -485.4 | 2.7 |

| China | 1.9 | 111.0 | 1.0 |

| Mexico | 1.8 | -5.2 | -0.1 |

| Other countries | 20.5 | -39.0 | -13.1 |

| Total | 102.3 | -15.8 | -19.3 |

| FDI sources | |||

| United States | 26.8 | -26.9 | -9.9 |

| Netherlands | 13.0 | 19.5 | 2.1 |

| Luxembourg | 7.8 | 90.9 | 3.7 |

| Australia | 5.0 | 1896.4 | 4.7 |

| United Kingdom | 4.2 | -59.8 | -6.2 |

| Brazil | 2.1 | -10.9 | -0.3 |

| France | 2.0 | -36.8 | -1.2 |

| Barbados | 1.3 | 293.0 | 1.0 |

| Hong Kong | 1.3 | -215.3 | 2.4 |

| Germany | 0.8 | -47.6 | -0.7 |

| Other countries | 0.2 | -98.5 | -13.4 |

| Total | 64.6 | -21.5 | -17.7 |

Source: Statistics Canada, Table 36-10-0473-01. Retrieved in May 2023. Calculation of the OCE.

It should be noted that both CDIA and FDI flow data reflect the immediate destination/investor information and refer to the last country through which the investment transited before reaching its destination. This is different from data based on the ultimate destination/investor which are more accurate but not always available. As a result, flow data may not accurately reflect investments from countries that invest via intermediaries (e.g., China or Japan) or that act as intermediaries (e.g., the Cayman Islands or Barbados). For more details on the difference between immediate and ultimate destination/investor, see Chapter 2 of Canada’s State of Trade 2021.