Extreme levels of household debt are common across the developing world. This is especially true in rural economies, where households face significant income volatility, but lack access to basic financial tools — such as insurance or futures contracts — that could reduce vulnerability to recurring income shocks.

In India, where over-indebtedness among rural households has been an important issue for decades, the government resorted to an unusually bold policy response. Prompted by a highly visible increase in farmer suicides, most notably in the Vidarbha region of Maharashtra, and a wave of defaults among microfinance borrowers, the Government of India embarked on what was perhaps the largest household level debt relief program in history. Announced in then finance minister Pranab Mukherjee’s budget speech on February 28, 2008 India’s Agricultural Debt Waiver and Debt Relief Program for Small and Marginal Farmers, cancelled the outstanding debts of 45 million rural households across the country, amounting to approximately 1.7% of India’s GDP.

While the benefit of debt relief programs to individual households can be substantial, their merit as a tool to improve household welfare in the long run remains highly controversial. Proponents of debt relief argue that extreme levels of household debt are likely to distort investment and production decisions, so that debt relief holds the promise of improving the productivity of beneficiary households. Critics of debt relief, on the other hand worry that it is difficult to “write off loans without also writing off a culture of prudent borrowing and repayment”1. If debt relief changes expectations and borrower behavior, they argue, bailouts may in fact lead to widespread moral hazard and more severe credit rationing in the future. Although both views can appeal to a foundation in economic theory, there exists surprisingly little evidence on how indebtedness, and hence debt relief, affect access to credit and economic decisions at the household level. India’s experiment with debt relief gives us a chance to bring empirical evidence to bear on this debate.

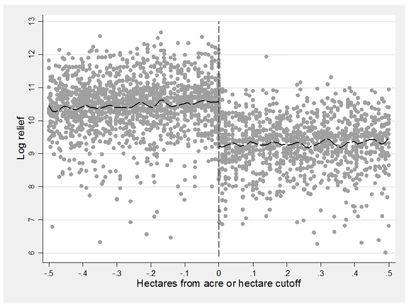

In a recent paper, I use a survey of 2,897 beneficiary households of India’s debt relief program to provide direct evidence on the impact of debt relief on the subsequent economic decisions of beneficiary households. The research design takes advantage of the fact that (in contrast to any previous debt relief initiative in India) eligibility for the program depended on how much land a household had pledged as collateral when it took out the loan: small farmers who had pledged less than 2 hectares got a 100% waiver, while households who had pledged more than 2 hectares were eligible for only 25% of relief, conditional on repaying their remaining balance. I use this cutoff (see Figure 1) as a source of quasi-random variation in debt relief amounts and estimate the causal impact of debt relief using a ‘sharp’ Regression Discontinuity Design that compares economic outcomes for households in the close vicinity of the eligibility threshold. The task of constructing a sample frame was made easier by the fact that, as a transparency measure, banks were required to disclose complete beneficiary lists of the program. This enabled us to identify all bailout recipients in several rural districts of the western Indian state of Gujarat (44,135 households) of which we interviewed households within a band of +/- .5 hectares of the program cutoff.

Figure 1: Discontinuity in debt relief at the program cutoff

So what happens to a household that has its entire debt cancelled overnight? The intention of the program was that debt forgiveness would not only lower oppressively high debt burdens, but operate like a personal bankruptcy settlement and provide households with a “fresh start” by clearing collateral and enabling new borrowing to finance productive investment. The results presented in the paper suggest that the program was successful along only one of these dimensions. Debt relief led to a substantial and persistent reduction of household debt. Even one year after the program was, beneficiaries of unconditional debt relief were approximately Rs 25,000 ($464 or 50% of median annual household income) less indebted than households in the control group. However, the results also show that, by and large, the program did not manage to reintegrate recipient households into formal lending relationships. Despite the fact that banks were required to make bailout recipients eligible for fresh loans, a large fraction of households do not use their freed collateral to access new loans. Evidence on loan applications after the program suggests that this is unlikely to be due to changes in the supply of credit. The absence of new borrowing among debt relief recipients is directly reflected in household investment and productivity –beneficiary households reduce their investment in agricultural inputs (which tend to be largely credit financed) and suffer a corresponding, economically significant decline in agricultural productivity.

There are two potential explanations for the observed decline in investment and productivity among recipients of debt relief. First, although debt relief had the immediate benefit of reducing the debt burden of recipient households, it also disrupted and in many cases ended long-standing banking relationships. Households who qualified for a 100% waiver typically had their account closed as a result and faced substantial fixed costs of restoring the credit relationship. This is particularly important given that many households derive significant value from banking relationships. For example, many households reported that –in the absence of debt relief — they largely depended on partial settlements to finance production (they negotiate partial settlements of to access new financing). In many cases, debt relief eliminated this financing option.

Second, the program applied only to defaulters so that appearing on the list of beneficiaries may not have been an unambiguously positive thing if it meant social stigma and future credit constraints as a result of being identified as a defaulter. Indeed, many beneficiary households in the study reported that they are concerned that qualifying for debt relief is a short term benefit that would make it significantly more difficult to obtain credit in the future. The patterns of post-program investment among bailout recipients are consistent with the anticipation of borrowing constraints (for example, ex-post investment among debt relief beneficiaries is not only lower but also more strongly correlated with household income and pre-program wealth).

What can these results teach us about designing more effective debt relief programs? First, it is important to note that the program was actually successful in reducing the debt burden of individual households and therefore did have a direct positive welfare effect. However, the program seems to have been largely unsuccessful at re-integrating households into formal credit relationships and removing disincentives for productive investment. This suggests that if debt relief is to encourage investment, debt forgiveness should be accompanied measures to restore banking relationships. By the same token, the results indicate that among the sources of investment constraints, expectations about future access to credit are as important as the disincentives generated by ‘debt overhang’ arising from high levels of inherited debt. Hence, a bailout designed to encourage new investment is likely to be effective only if it is implemented in a way that credibly improves households’ long term expectations about access to finance.

Finally, it is worth noting that these results can tell us something about the effect of debt relief on household investment and productivity, but cannot say much on the effect of a large-scale bailout on moral hazard and the supply of credit. Answers to survey questions about the perceived conditionality of different debt contracts suggest that this is a potential channel through which the bailout may induce moral hazard. However, in the absence of data on actual re-defaults after the program, this should be interpreted with caution. In related work we use data for debt relief, credit and loan performance in all districts of India to shed light on these important questions. More on this soon — watch this spot.

Figure 2: Survey household in Kheda district, Gujarat, India

1 “Waiving, not drowning: India writes off farm loans. Has it also written off the rural credit culture?” The Economist, July 3, 2008.

Join the Conversation