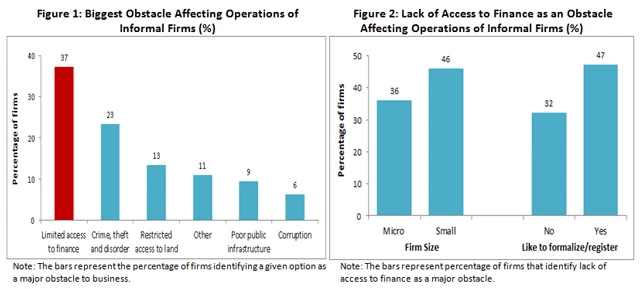

Informal economies are a significant part of developing countries across the world and according to some estimates can represent around 60 percent of countries’ official GDP (Schneider, et al. 2010). IFC estimates suggest that some 80 percent of micro, small, and medium enterprises in emerging markets and developing countries are informal today. Access to finance is by far the biggest obstacle these firms face (Figure 1). This obstacle is more acute for firms that would like to register, and it becomes critical as firms grow in size (Figure 2). Considering that about two-thirds of full-time jobs in developing economies are provided by such firms, it is essential to better understand issues around access to finance for informal firms. A paper that I recently wrote on the subject (Farazi 2014) as part of the work on the 2014 Global Financial Development Report is an attempt in this direction.

How does a typical informal firm look like, and what is its use of finance? As illustrated in Table 1, most informal firms have no more than 5 employees. The firms are less than 11 years old and majority of firm owners have some form of educational or vocational training. Very few firm owners have jobs in the formal business, implying that their informal business is their main source of income. Firms report very low use of loans and bank accounts and a significant majority finance their day-to-day operations and longer term financing through sources other than financial institutions (internal funds, moneylenders, family and friends). On average, most firms would like to register but don’t do so as it will require them to pay taxes and they state that relatively easier access to finance would be the most important benefit they could obtain from registering.

To identify the most important characteristics of informal firms that are associated with higher use of financial services I conducted a multivariate regression analysis in my paper. The results show that firm size, the level of education of the owner and whether the owner has a job in the formal sector are significantly associated with financial inclusion of informal firms. Micro firms vis-à-vis small firms have lower use of bank accounts and rely less on banks for working capital financing. Size is not significantly associated with the use of loans. Owner’s level of education and whether he/she has a job in the formal sector are positively associated with the use of bank accounts and negatively associated with the use of internal funds and financing from family and moneylender for working capital. Higher education levels of owners are also positively associated with the use of loans by informal firms.

The results reported above do not provide causal evidence, but they highlight some of the important features of informal firms that both researchers and policy practitioners can potentially focus on when analyzing financial inclusion for informal firms. Based on my basic analysis I would be inclined to say that policy interventions that focus on providing educational and vocational training to owners of informal firms and strengthen their ties with the formal sector by providing job or internship/apprenticeship opportunities can potentially improve financial inclusion of informal firms. However, as stated above there is a need for more thorough analysis. A lot of research in recent years has been done on understanding how informal firms can be encouraged to formalize. Some of this research indicates that lowering initial registration costs and providing information on registration procedures have only small effects on firm formalization (Bruhn 2013; de Andrade et al. 2013; De Giorgi and Rahman 2013). In ongoing research for the World Bank, Campos, Goldstein, and McKenzie find that the variable costs associated with becoming formal, such as tax payments, may be comparatively more important for informal firms. Unless these firms grow and become sufficiently profitable to cover such costs, it would be difficult for them to enter the formal sector. Enhancing financial inclusion of informal firms interested in registering can potentially help them grow and pave their path toward formalization (Campos, Goldstein, and McKenzie 2013).

References:

Bruhn, Miriam. 2013. "A tale of two species: Revisiting the effect of registration reform on informal business owners in Mexico", Journal of Development Economics, 103, 275–283

de Andrade, Gustavo Henrique, Miriam Bruhn and David McKenzie. 2013. "A Helping Hand or the Long arm of the Law? Experimental Evidence on what Governments can do to Formalize Firms." Policy Research Working Paper, World Bank, Washington, DC.

Campos, Francisco, Markus Goldstein, and David McKenzie. 2013. "Business registration Impact Evaluation in Malawi." Unpublished paper, World Bank, Washington, DC.

De Giorgia, Giacomo, and Aminur Rahman. 2013. "SME’s Registration Evidence from an RCT in Bangladesh." Economics Letters ISSN 0165-1765

Farazi, Subika. 2014. "Informal Firms and Financial Inclusion: Status and Determinants", Policy Research Working Paper 6778, World Bank, Washington, DC.

Schneider, Friedrich, Andreas Buehn and Claudio E. Montenegro. 2010. "Shadow Economies All over the World, New Estimates for 162 Countries from 1999 to 2007." Policy Research Working Paper 5356, World Bank, Washington, DC.

World Bank. 2013. "Global Financial Development Report 2014: Financial Inclusion". Washington, DC.

Join the Conversation