Financial market report for March 8, 2011

1) …. Introduction

Today the US Dollar started to rally as stocks surged in advance of a major sell off. A global stock, bond and currency rout is underway, which will result in a a global sovereign debt crisis, as well as a dollar liquidity crisis, ending in Götterdämmerung, that is an investment flameout.

2) … Today’s stock market rally was most likely a surge before a major turn lower.

Airlines, FAA, 5.1%; Airlines were the first stock sector to be destabilized by QE 2 as oil prices roared higher; Airline shares rose today as short sellers took profits.

Turkey, TUR, 4.1%; Turkey is the poster nation for hot money flows, and carry trade investing. Investors massively deleveraged out of Turkey with the announcement of QE 2; today Turkey rose as short sellers took profits.

Homebuilding, ITB, 4.0%; homebuilding stocks rose strongly immediately before the February 22, 2011 stock market sell off when seigniorage failed; today’s rise suggests another fall lower is imminent.

Thailand, THD, 3.6%; Thailand rose strongly just before the January fall in emerging market stocks; today’s rise suggests another fall loer is imminent.

South Korea Small Caps, SKOR, 3.6, EWY, 1.6%; South Korea small caps are the very definition of stimulus money flowing in and out of quantitative easing; their rise today suggests that a market turn is at hand.

Indonesia, IDX, 3.0%; Indonesia stocks rose strongly immediately before the emerging markets turned lower in January; today’s rise suggests that another fall lower is imminent.

India Small Caps, SCIN, 2.8%, INDY, 2.3% India Small Caps and India, are another poster nation for QE Stimulus; their rally communicates a fall lower is at hand.

Transportation, IYT, 2.8%; transportation shares rose to the middle of a broadening top pattern.

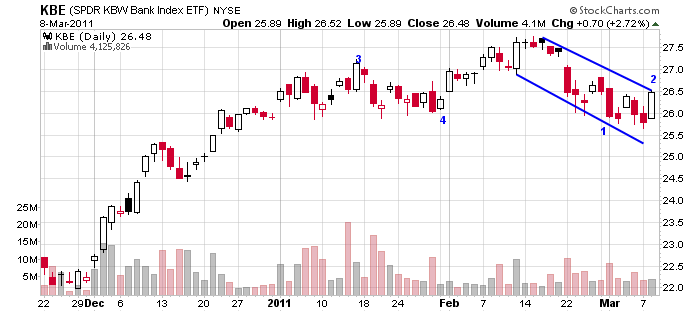

Banks, KBE, 2.7%; banks rose, cresting up into an Elliott Wave 2 up; their rise had nothing to do with rumored dividend increases, rather it was simply a rise up so that they could fall lower once again. Today’s rise was profit taking for short sellers.

Small Cap Industrial, XLIS, 2.1%

Financials, XLF, 2.1%

Small Cap Health Care, XLVS, 1.7%; this is a new rally high.

Taiwan, EWT, 1.6%; these Asian tigers are resetting for a fall lower.

Small Cap Consumer Discretionary, XLYS, 1.6%; the small cap consumer discretionary shares fell fast and hard on February 22; these will be one of the fastest fallers in the Age of Deleveraging as they are critically dependent upon easy to obtain low cost credit, which will simply not be available very soon.

Small Cap Information Technology, XLKS, 1.6%; the failed seigniorage of the Apple Ecosystem, will send these shares plummeting rapidly.

Russell 2000, IWM, 1.6%; the Russell 2000, like so many of the ETFs shows a bear flag pennant.

Pharmaceuticals, XPH, 1.5%, Pharmaceuticals have lost their Patents and are in a sharp sell off.

Russell 2000 Growth, IWO,1.5%

Water stocks, FIW, 1.5%

Emerging Market Small Cap Dividend, DGS, 1.5%

China All Caps, YAO, 1.5% China shares crested up into an Elliott Wave 2 high preparing them for a sell off.

Small Cap Revenue, RWJ, 1.4%

Environment Services, EVX, 1.4%

Industrial, IYJ, 1.4% Dow theory holds that the Industrial shares, IYJ, and the Transportation shares, IYT, make market turns together; both rose today, they will be falling lower together this week.

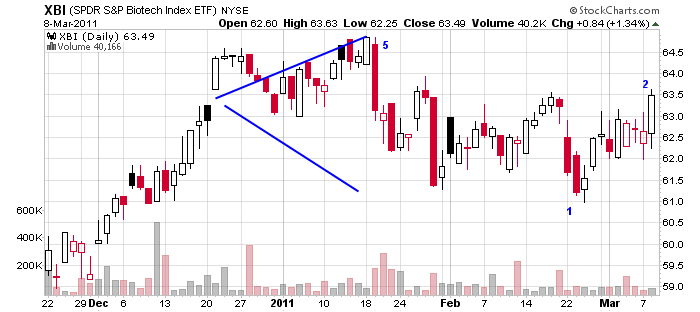

Biotechnology, XBI, 1.4%; the biotechnology shares rose to the middle of a broadening top pattern of which Street Authority relates when you see the broadening top, the market will eventually drop.

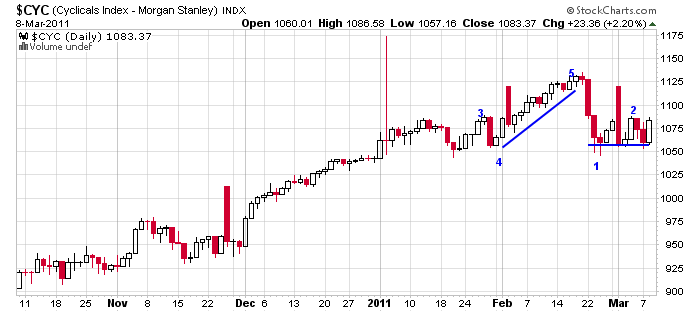

Morgan Stanley Cyclical Index, $CYC, 2.2%; these rose to the edge of a massive head and shoulders pattern.

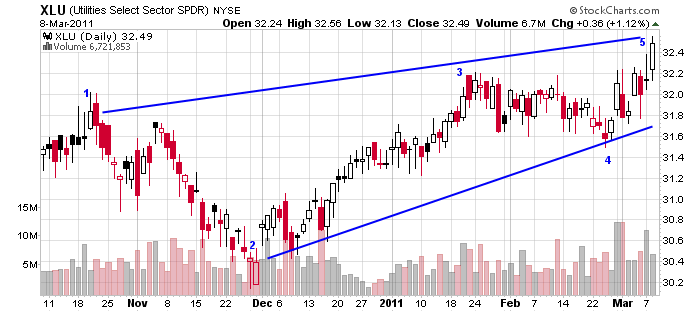

Utilities, XLU, 1.1% rose to a new high to close just below 32.50. They have crested up into an Elliott Wave 2 High just like the S&P, as is seen in the S&P Weekly. SPY Weekly.

The S&P, SPY, closed at 132.58, at the middle of a broadening top pattern, diamond triangle, consolidation pattern, that goes back to132.27 on February 9, 2011.

Stocks trading up today included the following. Retailer Advanced Auto Parts, AAP; it was one of those stocks, like BE Aerospace, BEAV, which were deleveraged early on by quantitative easing; but Sonic Automotive, SAH, being awesomely indebted, traded like Junk Bonds, JNK, and moved to a new high at 15.18.

Noteable fallers of the day included Natural Gas Partnership, Cheniere Energy Partners, CQP, Western Refining, WNR, Natural Gas: Chesapeake Energy Producer, CHK, Gold Mining Company Nevsun Resources, NSU, Gold Mining Shares, GDX,

Gold mining shares, GDX, disconnected from gold, GLD, and fell lower today, as is seen in the chart of GDX:GLD, Gold shares always turn lower with the 30 Year US Bond at market turns, this is communicated in the chart of the HUI Precious Metal Mining Stocks Relative To US Treasuries, $HUI:$USB.

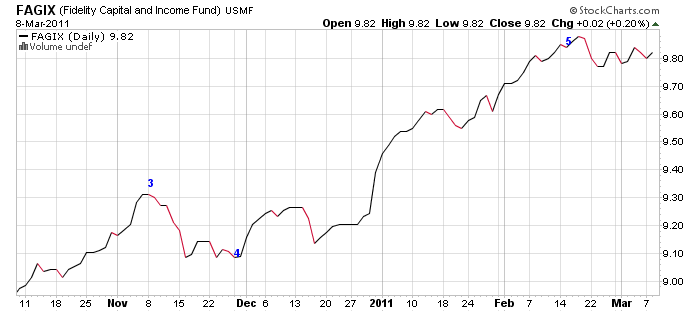

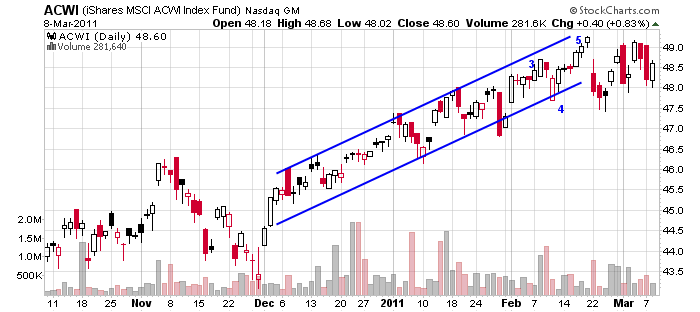

3) …. Seigniorage, that is moneyness, failed on February 22, 2011 as the value of distressed securities, like those held in Fidelity Mutual Fund FAGIX turned lower in value. It was at this time that quantitative easing failed and inflation destruction commenced turning world stocks, ACWI, lower.

Urban Dictionary defines inflation destruction as the fall in investment value that accompanies derisking and deleveraging out of investments that were formerly inflated by money flows to, and carry trade investing in, high interest paying financial institutions, profitable natural resource companies, and high growth companies.

A dollar liquidity crisis is coming from the exhaustion of quantitative easing.

Stocks, bonds, and commodities are all going to be falling lower as the monies that the US Federal Reserve are now pumping into the global economic system fail to stimulate and actually turn toxic.

Chris Martenson in Zero Hedge Blog relates: “The Fed has been dumping roughly $4 billion of thin-air money into the US markets each trading day since November 2010. The markets, all of them, are higher than they would be without this money. $4 billion per trading day is an enormous amount of money. It’s gigantic by historical standards.”

The bond vigilantes have seized control of interest rates globally and a massive sell of bonds is underway.

This commenced when the US central bank announced that it is going to print money out of thin air and then actually did so, the bond vigilantes went to work, calling the interest rate on the 30 Year bond, $TYX, and the interest rate on the 10 Year US Government Note, $TNX, higher, resulting in a steeping 10 30 Yield Curve, $TNX:$TYX, and a flattening 30 10 Leverage Curve, $TYX:$TNX.

The US Federal Reserve’s monetization of debt has resulted in a tremendous loss of value in government bonds, as is seen in the chart of the Flattner ETF, FLAT together with EDV, and TLT …. FLAT, and EDV, and TLT. The Feds actions have resulted in debasing the US Dollar, $USD, which in turn gave an explosive seigniorage and birth to oil, USO, as a premier currency, along with gold, GLD, and silver, SLV.

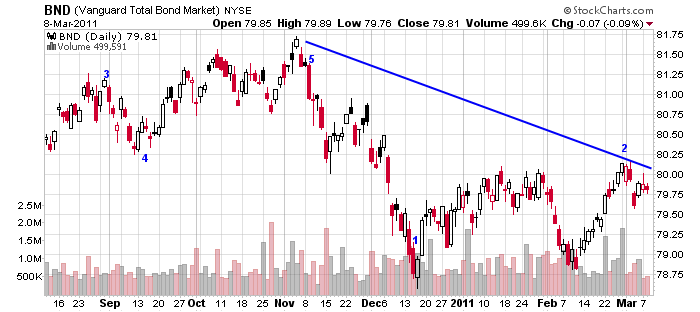

Bonds, BND, have entered an Elliott Wave 3 Decline.

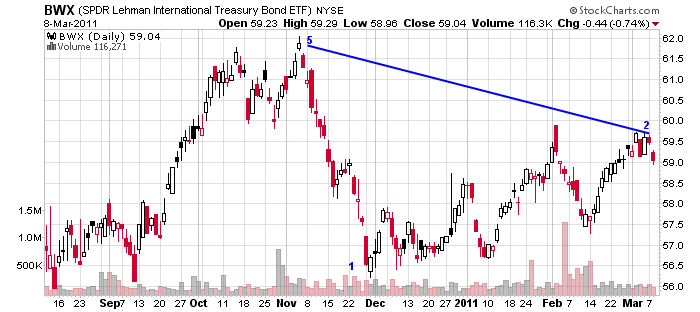

World Government bonds, BWX, and International Corporate Bonds, PICB, have entered an Elliott Wave 3 Decline as well. Today’s fall lower in world government bonds suggests that a sovereign debt crisis has commenced.

The failure of seigniorage and leverage is seen in the turning lower of world stocks relative to world government bonds, VT:BWX, and the turning lower of US stocks relative to the 10 Year Bond, VTI:TLT.

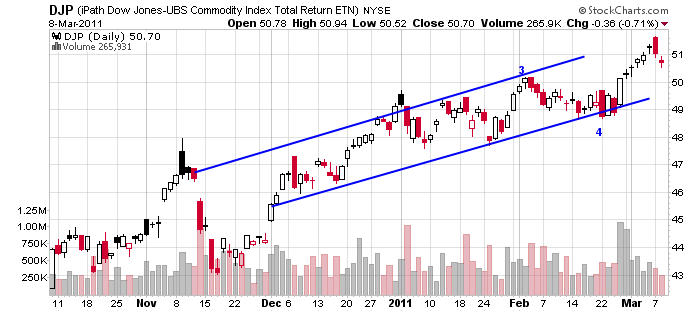

Commodities and US Commodities turned lower today on failed seigniorage.

Commodities, DJP and US Commodities, USCI, turned lower as seigniorage, that is the value of the distressed securities at the Fed, approximated in value by the mutual fund FAGIX, together with the 30 Year US Government Bonds, EDV, adn the 10 Year US Government Notes, TLT.

The turn lower in Base Metals, DBB, reflects the death of the old seigniorage, that is the moneyness that came via Neoliberalism and the Milton Friedman Free To Choose Floating Currency Regime. Please notice the intensity of fall is greater in Material, XLB, then less in US Basic Materials, IYM, and now just picking up in the base metals, DBB. Speculators, that is the hedge funds, could hold on longer in the commodities than the investors in commodity stocks, before being dislodged by inflation destruction. The question now arises, will the rate of fall in the base metal commodities exceed the rate of fall in the stocks?

Gasoline, UGA, traded 2.1% lower today.

Agriculture Commodities, JJA, traded 1.2% lower today.

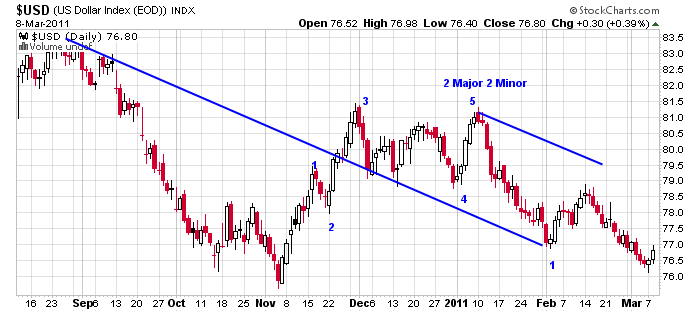

The US Dollar rose today as dollar ill-liquidity and demand for dollars commenced.

Bloomberg reports: “The US dollar, $USD, (traded by the 200% ETF, UUP), may reverse declines that have seen the currency drop 3.5% this year after bets on its depreciation against its major counterparts climbed to the most on record, according to UBS AG. Bets on the dollar weakening, so-called net shorts, surged in the week ended March 1 to the highest since the CFTC began publishing the data in 2003. “Investors should prepare for possible unwinding of these negative bets against the dollar, which are extreme at the moment.”

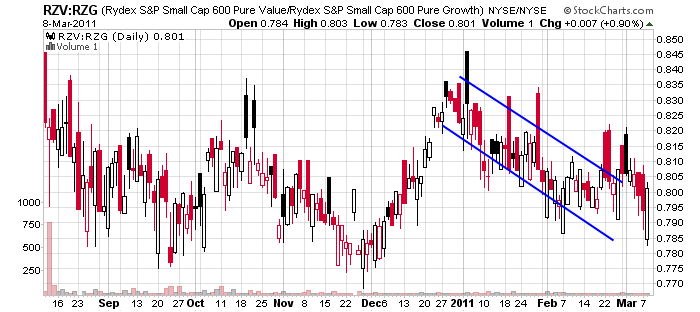

Small Cap Pure Value, RZV, 2.6%; today’s rise was the likely completion of a bear flag pennant, preparing these stocks to fall lower; this rise normally occurs with a rise in financial shares; this rise is a surge in dollar buying that precedes a strong selling of world currencies, DBV, emerging market currencies, CEW, and commodity currencies, CCX; this will likely fall lower with stocks in the next few selling sessions. Trading chart patterns relates a Bear Flag is a sharp, strong volume decline, several days of sideways to higher price action on much weaker volume followed by a second, sharp decline to new lows on strong volume. Bearish flags are comprised of higher tops and higher bottoms. “Bear” flags also have a tendency to slope against the trend. Yes we are likely to see competitive currency deflation, that is competitive currency devaluation come to other currencies at this time as the FX currency traders expand their global currency war against the world central banks for control of the world’s people and resources.

This reversal in the US Dollar, $USD, seems consistent with the fact that the Currency Leverage Curve Daily, RZV:RZG, is now falling lower in its channel again; and that the Currency Leverage Curve Weekly, RZV:RZG Weekly, is now turning lower again for the second week.

One can create track these currencies FXA, FXE, FXM, FXC, ICN, FXB, FXS, SZR, FXF, CYB, BZF, XRU, FXY, BNZ, DBV, and CEW, using this Finviz Screener which shows that the New Zealand Dollar, BNZ, traded up with the US Dollar, as investors took profits on their short sales.

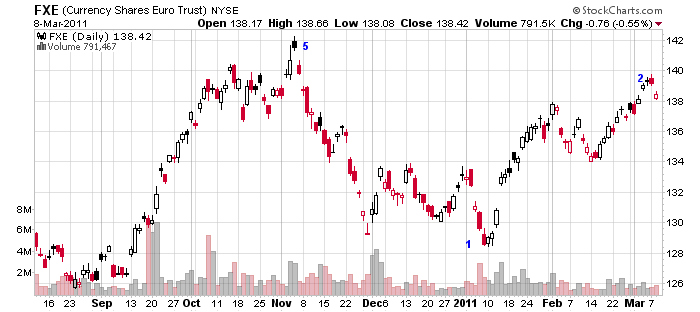

The Russian Ruble, XRU, and the Swiss Franc, FXF, the Swedish Krona, FXS, and the Euro, FXE, were today’s loss leaders.

The Euro, FXE, traded lower at 138.42 today having risen from 119 in June with the announcement of the EFSF Authority. Might the EFSF Monetary Authority Rally be over? I say so!

Martin Sibileau of a A View From The Trenches, relates: “In summary, we think there is no buying opportunity here and we even fear that gold may soon no longer resist the deleveraging forces at play, if Greece’s default becomes imminent, once the EU Council meeting of March 24-25 ends without clear resolution on the future of the EFSF. Indeed, if the situation deteriorates, counterparty risk will increase exponentially and liquidity will be sought everywhere. Gold would also be a victim.”

“We have already dealt here with counterparty risk in sovereign default swaps. This is something regulators have not addressed at all and is in fact the weakest link. Will we see it escalate in 2011? We have no idea, but we must be prepared and therefore, we briefly elaborate on it below.”

“When a bank sells a credit default swap on a sovereign within the Euro zone, say Greece, it promises to pay, if default occurs, par on the protected notional under the contract. But that notional is denominated in US dollars. As you can imagine, even if that default is caused by a strong Euro, at default, there will be a rush to USD liquidity, as those financial institutions that sold protection on Greece’s sovereign risk need to buy US dollars to deliver on their promise to pay. Therefore, the strength in the Euro that we currently see can swiftly turn into weakness, because in the presence of jump-to-default risk (i.e. right before the actual default.”

“Could this actually happen? It all depends on what the EU Council decides on March 24-25. Until then, in our personal accounts, we want to hold cash and gold. No stocks or bonds. Not even energy stocks or gold mining stocks, for they end with the word “stocks” and that will be enough for margin clerks to sell them (the case was made yesterday, as both gold and oil managed to make intraday highs and yet, the respective energy and mining stock ETFs sold off).”

“Lastly, it will be very useful to understand that for this to happen, it is not even necessary that the ECB actually hikes rates. In fact, we think there is a chance they won’t. However, with last week’s threat, the technical damage has been done.”

“Now, at this point, it should be clear that this counterparty risk will violently transform into systemic risk. Funding in US dollars, within the Euro zone will be limited, pushing Libor higher and leaving the Fed without a choice. The Fed will need to extend currency swaps to the European Central Bank. Why? Because at the end of the day, the ECB will have de facto renounced its monetary authority. The funds that Trichet refused to print on March 3 would eventually be lent, in multiples, by the Fed to European (and non-European) banks. Will Congress allow this? Until this point, gold would be under a lot of pressure. But it would soon become clear that the Fed cannot bail out the entire world and gold would then reach unthinkable highs.”

Of note the USD/JPY has been increasing in value since the announcement of QE 2 as seen in Yahoo Finance Chart of USDJPY this is reflected in the ETF JYN falling lower.

4) ,… Conclusion

The world is passing from ….. The Age of Leverage characterised by debt expansion, credit liquidity, stability, economic growth and expansion and prosperity …. and into ….. The Age of Deleveraging characterised by inflation destruction, debt deflation, credit ill-liquidity, instability, economic contraction and austerity.

Freedom’s Lighthouse reports that Herman Cain closed his We Must Become The Defending Fathers speech delivered at the Iowa Faith & Freedom Coalition gathering by saying that he has a “breaking news announcement” for President Obama and the liberals all across this great nation: “The United States of America is not going to become the United States of Europe – not on our watch!”

But such rhetoric will ring hallow, as Leaders are quietly announcing Framework Agreements for both political order and state corporate prosperity. For example on February 4, 2011, The Prime Minister of Canada website released the Declaration by the Prime Minister of Canada and the President of the United States of America of a framework agreement for Perimeter Security and Economic Competitiveness. And also on February 4, 2011, The Prime Minister of Canada website released the the announcement of another framework agreement establishing The Bilateral Regulatory Cooperation Council, RCC. And Ireland was forced to take the EU and IMF bail-out package on November 22, 2010.

In announcing these Framework Agreements, the Leaders are waiving national sovereignty and establishing themselves as sovereign authorities; one is no longer a citizen of a sovereign nation state, rather one is a resident living in a region of global economic governance. The word, will and way of the leaders is sovereign replacing constitutional law as well as the traditional rule of law.

The report of Jordan Shilton in WSWSorg article Irish Labour Party and Fine Gael commit to savage austerity is not rhetoric, like that of Mr. Herman Cain. The austerity of global economic governance, that came by EU and IMF bailout, is going to be applied by the new government in Ireland.

A new political and economic paradigm, that being rule of the sovereigns, will emerge out of Götterdämmerung, an investment flameout, where a Chancellor, that is a Sovereign, and a Banker, a Seignior, will arise and govern through global corporatism. Such leadership may come out of Germany heralding the strength of a revived Roman Empire, as Germany has its ancestral roots in that former empire. National leaders will waive national sovereignty and announce Framework Agreements. These Agreements will appoint stakeholders to oversee regional economic governance. The two leading Sovereigns will provide a new seigniorage, that is a new moneyness, with stimulus for global corporations, and austerity and democratic deficit for all peoples

In an inflation destruction, and in a debt deflation, that is a currency deflation world, wealth can only be preserved by investing in and taking possession of physical gold, GLD, and silver, SLV.

5) … In today’s News

Nigerian Tribune reports Naira Weakens On Strong Dollar Demand

The naira weakened slightly against the United States dollar on the interbank market, on Monday, as demand for the greenback remained strong and inflows from energy companies decreased.

The currency closed at N154.30 to the dollar, compared to N154.25 on Friday.

The Central Bank of Nigeria (CBN) sold $350 million at N150.68 to the dollar at its bi-weekly auction on Monday, marginally lower than the 152 million demanded, but an increase compared to the $250 million sold at N150.71 a dollar at last Wednesday’s auction.

Traders said demand remained strong from some lenders, who were covering their position and supplying bureaux de change outlets.

An oil firm, Exxon Mobil, sold about $49 million to some lenders on Monday, but traders said dollar liquidity remained tight, as most of oil multinationals has concluded their month-end dollar sales.

“We are hopeful that there could still be some inflow from some energy firms to help provide the needed dollar liquidity in the market, otherwise, the naira will continue to depreciate,” one dealer said.

The bulk of dollars traded on the interbank market came from energy companies, as banks were not allowed to trade dollars purchased at the official window among themselves.

Vietnam Finance News reports Hanoi dollar transactions halted unexpectedly

Foreign exchange points in the northern capital city of Hanoi unexpectedly stopped transactions of U.S. dollar Monday afternoon even though commercial banks asserted they had yet to formulate a policy on controlling their foreign exchange networks.

Early in the morning, foreign exchange points remained in normal operation, announcing the trading rate at VND21,500-21,680/US$1. They, however, refused to buy the dollar and stopped all dealings in the afternoon.

Ha Trung, a street well-known for gold and foreign currency trading, looked duller than usual in the morning. While many shops traded mainly gold, especially jewelry gold, others suspended all foreign currency transactions.

Bloomberg reports Greek Bond Yields, Swaps Climb to Records Before EU Leaders Discuss Crisis.

Greek 10-year bond yields and credit-default swaps surged to a record as borrowing costs increased at a debt sale and before European leaders begin meetings aimed at containing the sovereign debt crisis. Spanish bonds also slid as the government sold debt through banks. Greek bond losses extended declines to a ninth day after the nation’s credit rating was cut by Moody’s Investors Service yesterday. Portuguese 10-year bonds fell for a second day before a notes auction tomorrow. German 10-year bonds dropped amid speculation the nation’s economic growth will add to pressure on central bankers to increase interest rates. “There is quite a lot of peripheral supply that needs to be digested and apparently we’re struggling to find more buying interest at these levels,” said Marcel Bross, a fixed-income strategist at Frankfurt-based Commerzbank AG. “We have these important meetings coming up, where we see some potential for disappointment.” The yield on 10-year Greek bonds jumped as much as 52 basis points to 12.85 percent, the most since Bloomberg began collecting the data in 1988, with the increase in yields the biggest since Oct. 27. The extra yield investors demand to hold the securities instead of German bunds widened to as much as 956 basis points, the most since Jan. 10. The euro fell 0.4 percent to $1.3912. Credit-default swaps insuring Greek government bonds rose five basis points to an all-time high 1,037 basis points, meaning it costs $1.04 million annually to insure $10 million of debt for five years. (Hat Tip to Gary of Between The Hedges)

Bloomberg reports Confidence at U.S. Small Companies Climbs to Three-Year High, Survey Shows. Confidence among U.S. small companies rose in February to the highest level in three years as hiring and sales expectations increased, a survey showed. The National Federation of Independent Business’s optimism index climbed to 94.5, the highest since the recession began in December 2007, the Washington-based group said today in a statement. The reading compares with the average 100.7 during the previous expansion that started in November 2001. Hiring plans rose to the second-highest level since September 2008, a sign employment may pick up in coming months. At the same time, earnings expectations remained negative, and fewer businesses said it was a good time to expand. (Hat Tip To Gary of Between The Hedges)

6) … Keywords; Dollar Liquidity Crisis, Liquidity Crisis, Seigniorage, Moneyness, Failure of Seigniorage, Sovereign Default Counter Party Risk, Sovereign Crisis, Sovereign Debt Crisis, Inflation Destruction, Competitive Currency Deflation, Competitive Currency Devaluation, Global Currency War, Morgan Stanley Cyclical Index, Monetization of Debt, Currency Debasement, Neoliberalism, Demand for Dollars,

Götterdämmerung, global sovereign debt crisis, global liquidity crisis,

Leave a comment